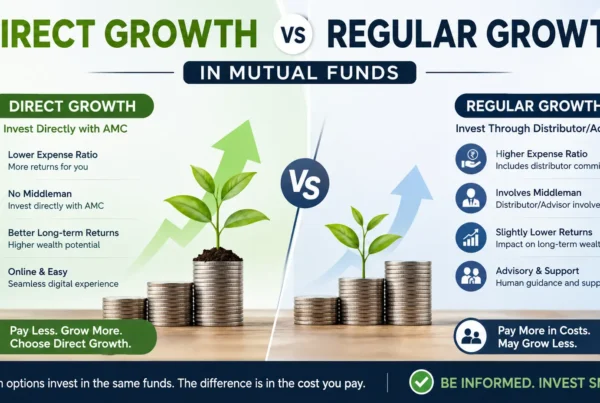

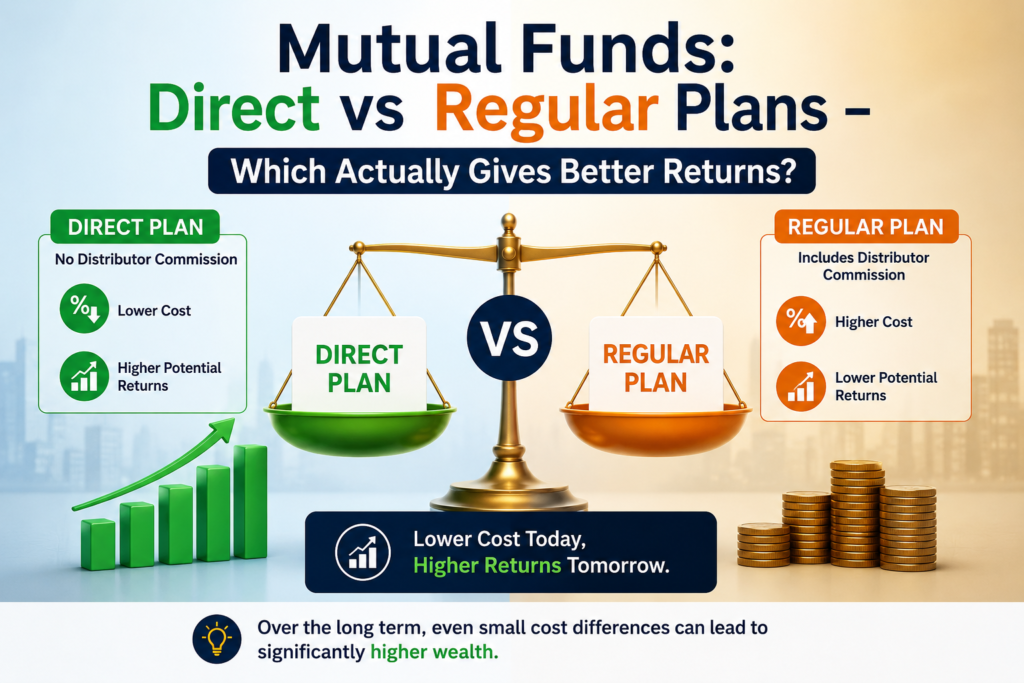

When comparing mutual funds direct vs regular plans, the difference in returns can be more significant than most investors realize. The key factor lies in the expense ratio—the fund’s total expenses relative to its assets under management. Direct mutual funds have a considerably lower expense ratio because they eliminate the middleman.

The difference between regular and direct mutual fund expense ratios typically ranges from 0.5% to 1%[-3]. Although this might seem minimal at first glance, regular vs direct mutual fund performance diverges substantially over time. In fact, if the Total Expense Ratio (TER) of a regular plan is 0.75% higher than that of a direct plan, the direct plan will deliver approximately 1% higher CAGR return. For the long term investor, this initially small percentage difference can ultimately result in a substantial gap of lakhs of rupees in the final corpus.

We’ve noticed that direct mutual funds consistently outperform their regular counterparts, with some cases showing returns as high as 1.83% per annum more compared to regular plans. As a result, direct funds maintain a higher Net Asset Value (NAV) than regular funds of the same mutual fund. In this article, we’ll examine the crucial differences between these two investment approaches and help you determine which option might better align with your financial goals.

Expense Ratio and Cost Structure

The financial impact of expense ratios forms the foundation of the direct vs regular mutual fund debate. Understanding this cost structure is essential for making informed investment decisions.

What is Total Expense Ratio (TER)?

Total Expense Ratio represents all costs associated with managing and operating a mutual fund. TER encompasses management fees, administrative expenses, legal fees, auditor fees, transaction costs, and other operational expenses. These costs are calculated as a percentage of the fund’s daily net assets and directly affect the fund’s NAV—the lower the expense ratio, the higher the NAV.

SEBI regulates the maximum TER mutual funds can charge, with limits varying based on the fund’s assets under management (AUM). For equity funds, TER caps range from 2.25% for funds with AUM below ₹500 crore to 1.05% for funds exceeding ₹50,000 crore. Debt funds have slightly lower caps, from 2.00% to 0.80% respectively.

Direct Plan: No Distributor Commission

Direct plans eliminate the intermediary between investors and fund houses. Since no third-party distributors are involved, these plans save on distribution costs and commissions. This absence of commission is the primary reason direct plans maintain lower expense ratios—typically 0.5% to 1.5% lower than their regular counterparts.

Furthermore, these savings are added back to the scheme’s returns, making direct plans potentially more profitable over time. The NAV of direct plans is consequently higher than regular plans of the same scheme, though the difference might initially appear marginal.

Regular Plan: Includes Advisor Fees

Regular plans include distributor commissions within their expense structure. These commissions typically range from 0.5% to 1.5% of the investment value. Regular plans create a distribution network by compensating intermediaries who connect investors with fund houses.

The commissions paid to distributors contribute directly to the fund’s expense ratio, potentially affecting overall returns. Therefore, regular plans generally have higher TERs since they must cover both management costs and distribution expenses.

Impact of TER on Investment Value

Even small differences in expense ratios can significantly impact investment growth over time. Consider investing ₹100,000 for 10 years with a 15% return—a direct plan would yield ₹441,143, whereas a regular plan would yield ₹404,555, representing a difference of ₹36,587 due to a mere 1% difference in expense ratio.

The impact becomes more pronounced with larger investments. A ₹10 lakh investment growing at 8% annually for 30 years would be worth ₹76 lakhs in a regular plan but approximately ₹1 crore in a direct plan with a 1% lower expense ratio.

This cost difference compounds dramatically over time because expense ratios are deducted from the fund’s returns daily, reducing the amount available for reinvestment. Consequently, investors must carefully weigh expense ratios alongside other factors like fund performance and management quality when selecting investments.

Returns Over Time: Direct vs Regular

The numerical advantage of direct plans becomes increasingly apparent when examining actual return data over time. While the expense ratio difference might seem minor initially, its impact on investment returns grows exponentially with time.

Annual Return Comparison: 5-Year Data

Real-world data shows direct mutual funds consistently outperform their regular counterparts. In some cases, direct plans have delivered as much as 1.83% higher annual returns compared to their regular versions. Even for conservative funds, the difference typically ranges from 0.69% to over 1% per annum.

A practical example demonstrates this difference: investing ₹20,000 monthly for five years (2014-2019) in a portfolio with 75% allocation to equity funds and 25% to debt funds showed notably higher returns in direct plans. The difference in the final portfolio value was substantial, even within this relatively short timeframe.

CAGR Impact: 0.5% to 1.5% Difference

The difference in Total Expense Ratio (TER) between regular and direct plans varies from 0.5% to 1.5%, depending on the fund type and AMC commission structure. Equity funds typically show larger differences than debt instruments like overnight or liquid funds.

This expense difference directly translates to CAGR (Compound Annual Growth Rate) differences. For instance, if a regular plan’s TER is 0.75% higher than its direct counterpart, the direct plan will yield approximately 1% higher CAGR return. Moreover, this return gap widens as the investment horizon lengthens.

Compounding Effect Over 10, 15, 20 Years

The true power of direct plans emerges during long-term investing. Consider these real examples:

- For a ₹10,000 monthly SIP over 15 years with a 12% assumed return (before expenses): the direct plan would yield approximately ₹50.2 lakhs while the regular plan would yield ₹46.5 lakhs – a difference of ₹3.7 lakhs.

- An investment of ₹3 lakhs growing at 18.65% in a direct plan versus 16.82% in a regular plan (1.83% difference) would create an additional wealth of ₹2.38 lakhs over 10 years, ₹8.11 lakhs over 15 years, and a remarkable ₹24.5 lakhs over 20 years.

Additionally, in another case study with a ₹10,000 monthly SIP for 10 years, the direct plan accumulated approximately ₹83.5 lakhs while the regular plan reached only ₹76.4 lakhs – a ₹7 lakh difference. If extended to 20 years with similar returns, the direct plan would create ₹19.5 crores versus ₹15.9 crores in the regular plan – an astounding ₹3.6 crore difference.

These examples illustrate how small percentage differences in returns, primarily resulting from lower expense ratios, can yield significantly different investment outcomes over extended periods.

NAV Differences and Their Implications

Net Asset Value (NAV) discrepancies between direct and regular plans reveal another critical dimension in the mutual fund selection process. Understanding these differences helps investors make informed decisions about their long-term financial goals.

Why Direct Plans Have Higher NAV

The Net Asset Value (NAV) of a mutual fund represents the per-unit market value of the fund’s securities. Specifically, NAV is calculated by dividing the market value of all securities held by the fund by the total number of outstanding units. Given that the Total Expense Ratio (TER) is adjusted directly from this NAV, plans with lower expenses ultimately maintain higher valuations.

Direct plans consistently show higher NAVs than their regular counterparts of the same scheme. This occurs because no commissions are paid to distributors or agents in direct plans, resulting in lower expense ratios. Conversely, regular plans must account for distribution costs, which are subtracted from the fund’s returns, leading to a reduced NAV.

The NAV difference, while seemingly marginal at first glance, continues to widen over time as the expense gap compounds. This creates a perpetual advantage for direct plan investors beyond the initial investment phase.

How NAV Affects Your Investment Growth

The higher NAV of direct plans translates directly into superior investment performance over time. Your investment value after purchase will always be greater in a direct plan compared to its regular variant, assuming all other factors remain constant.

A real-world example illustrates this impact perfectly. The ICICI Bluechip Fund’s direct and regular plans both started with identical NAVs of ₹18.55 in January 2013. However, by September 2022, the direct plan’s NAV had reached ₹74.40 while the regular plan stood at only ₹68.86.

This NAV disparity creates substantial differences in wealth accumulation:

- A ₹25,000 monthly SIP for 9 years would yield ₹63.8 lakhs in the direct plan versus ₹60.99 lakhs in the regular plan – a difference of approximately ₹3 lakhs (5%)

- For longer horizons of 25-30 years, the difference grows exponentially

- A ₹25,000 monthly SIP for 30 years with returns of 12% (direct) versus 10.5% (regular) would create a corpus of ₹7.8 crores versus ₹6.3 crores – an enormous shortfall of ₹1.5 crores (nearly 25%) in the regular plan

This growing NAV divergence stems from the compounding effect of expenses. Even a small expense difference of 0.5-1% annually can substantially impact your final corpus. Subsequently, as investment periods extend, the performance gap between direct and regular plans continues to widen.

Investor Control and Transparency

Beyond expense ratios and returns, the control over investment decisions also distinguishes mutual funds direct vs regular plans. The investment approach varies dramatically between these options, affecting both transparency and investor autonomy.

Direct Plans: Full Control and DIY Approach

Direct mutual funds empower investors with complete control over their investment decisions. In this Do-It-Yourself (DIY) approach, investors select funds based on independent research without relying on intermediaries. This hands-on method requires investors to conduct their own research, handle transactions themselves, and make decisions independently. Besides managing their portfolios actively, direct plan investors enjoy greater transparency with direct access to information regarding fund performance, portfolio holdings, and expenses. This approach primarily suits experienced investors who understand financial markets well and prefer cost-efficient investing. Certainly, the direct relationship with the Asset Management Company (AMC) ensures investors can independently evaluate fund managers’ portfolios and strategies.

Regular Plans: Advisor-Driven Decisions

Regular mutual funds operate through intermediaries such as financial advisors, brokers, or distributors. These professionals provide advice, insights, and solutions regarding portfolio balancing, investment strategy, and wealth creation. Mutual fund distributors offer valuable services including advising on scheme selection, submitting KYC documents, helping with the investment process, as well as generating account statements and processing redemption requests. Importantly, these advisors help avoid decisions based on emotional biases by developing investment strategies that balance risk and rewards. This advisor-driven approach particularly benefits beginners or investors seeking professional guidance.

Risk of Mis-selling in Regular Plans

Despite the advantages, regular plans carry risks of mis-selling. SEBI has identified mis-selling as a fraudulent practice, namely making false statements, concealing material facts or risk factors, and not ensuring suitability of schemes for buyers. In some cases, investors may be advised to invest in funds that bring better commissions for agents rather than those suitable for their needs. Above all, SEBI has proposed strengthening the mutual fund distribution system to prevent possible mis-selling by banks and national distributors. The regulator has suggested recording calls of relationship managers with customers for auditing and compliance purposes. Nevertheless, industry experts acknowledge that some amount of mis-selling cannot be completely eliminated.

Who Should Choose What?

Selecting between mutual funds direct vs regular plans largely depends on your investment knowledge, time availability, and personal preferences. Investor profiles play a crucial role in determining which approach might be most suitable.

New Investors: Why Regular May Be Safer

First-time investors or those unfamiliar with financial markets often benefit from regular mutual fund plans. These plans provide personalized financial advice with advisors assessing your risk profile, income, and future goals to build a well-balanced portfolio. Essentially, mutual fund distributors offer valuable services like suggesting suitable schemes, handling KYC documentation, and processing transactions.

Undeniably, when markets fall and investment values come under pressure, independent advice from a professional advisor can help you stay the course. Regular plans offer ongoing support through portfolio reviews, with advisors tracking your fund’s performance and suggesting changes to keep investments aligned with your goals. This emotional discipline during market volatility is particularly valuable for beginners.

Experienced Investors: Benefits of Direct Plans

Direct mutual fund plans suit investors who prefer controlling their finances and making investment decisions independently. If you have adequate knowledge to select good funds yourself or are willing to seek advice from a registered investment adviser for a fee, direct plans make perfect sense.

These plans reward self-discipline and long-term thinking by eliminating unnecessary costs. Tech-savvy investors already using online platforms or AMC websites find direct plans straightforward for investing, switching, and tracking mutual funds. Alternatively, experienced investors with proper market knowledge gain full control of their investments, requiring them to do their homework into studying funds.

Goal-Based Planning and Portfolio Monitoring

Goal-based investing identifies financial objectives, sets timelines, and invests regularly to reach them. Accordingly, your investment horizon should determine your choice between regular and direct plans.

For short-term goals like travel or school fees, debt funds or fixed deposits typically work best. Medium-term goals (3-5 years) might benefit from hybrid funds that balance growth potential with stability. Long-term objectives like retirement could utilize pure equity funds focused primarily on growth.

Both plan types can fit into goal-based strategies, depending on your monitoring capabilities. With direct plans, you must track performance yourself, unlike regular plans where advisors monitor and review your portfolio. Fundamentally, annual rebalancing of asset allocation ensures that as you approach your goal, you can lower equity exposure to protect gains.

Comparison Table

| Feature | Direct Plans | Regular Plans |

| Expense Ratio | Lower by 0.5% to 1.5% | Higher due to distributor commissions |

| Distribution Costs | No distributor commission | 0.5% to 1.5% commission included |

| NAV | Consistently higher | Lower than direct plans |

| Returns Difference | Up to 1.83% higher per annum | Lower returns due to higher expenses |

| Investment Control | Complete control (DIY approach) | Advisor-driven decisions |

| Portfolio Management | Self-managed | Managed through intermediaries |

| Transparency | Direct access to fund information | Information through advisors |

| Suitable For | – Experienced investors- Tech-savvy investors- Self-research capable investors | – New investors- Those needing guidance- Less experienced investors |

| Advisory Support | None included | Professional guidance included |

| Risk of Mis-selling | Minimal (direct investment) | Present due to commission-based selling |

| Example Returns (₹10,000 monthly SIP for 10 years) | Approximately ₹83.5 lakhs | Approximately ₹76.4 lakhs |

Conclusion

The debate between direct and regular mutual fund plans ultimately comes down to a trade-off between cost savings and professional guidance. Throughout this analysis, we’ve seen how direct plans consistently outperform regular plans due to their lower expense ratios. This difference might seem minimal initially—typically 0.5% to 1.5%—but compounds dramatically over time.

Consider the numbers: a difference of just 1% in returns can translate to several lakhs or even crores of rupees over investment periods of 15-20 years. This substantial gap exists because direct plans eliminate distributor commissions, allowing more of your money to work for you through the power of compounding.

The higher NAV values of direct plans further demonstrate their advantage. These values continue to widen over time, creating a perpetual benefit for direct plan investors beyond the initial investment phase.

Nevertheless, regular plans serve an important purpose for new investors. These plans provide valuable guidance from financial advisors who can help navigate market volatility, create balanced portfolios, and maintain emotional discipline during market downturns. This support justifies the additional expense for investors who lack market knowledge or confidence.

Experienced investors, however, will likely benefit more from direct plans. Those with adequate market understanding, research capabilities, and the discipline to stick with long-term strategies can maximize their returns by avoiding unnecessary expenses.

Your investment horizon also plays a crucial role in this decision. For long-term goals such as retirement planning, the cumulative effect of lower expenses in direct plans can significantly enhance your final corpus. Conversely, shorter-term objectives might benefit from the structured approach and professional oversight offered by regular plans.

Undoubtedly, both investment approaches have their merits. The choice between direct and regular mutual fund plans should align with your financial knowledge, time availability, and personal comfort with managing investments. What matters most is selecting the option that best supports your financial journey and helps you achieve your goals with confidence.