Imagine two friends — Rohit and Priya — both invest ₹10 lakh in mutual funds in 2010. Same amount, same broad market. Fifteen years later, Rohit’s portfolio has grown to ₹52 lakh. Priya’s? ₹61 lakh. They followed the same strategy, tracked the same index, rode the same bull runs and bear markets. The only difference? Priya paid a mutual fund expense ratio of 0.2% per year. Rohit paid 1.5%.

That 1.3% gap didn’t feel like much on a Tuesday afternoon in 2010. Over 15 years, it quietly swallowed ₹9 lakh of Rohit’s wealth — without a single notice, no SMS alert, no deduction visible in his statement.

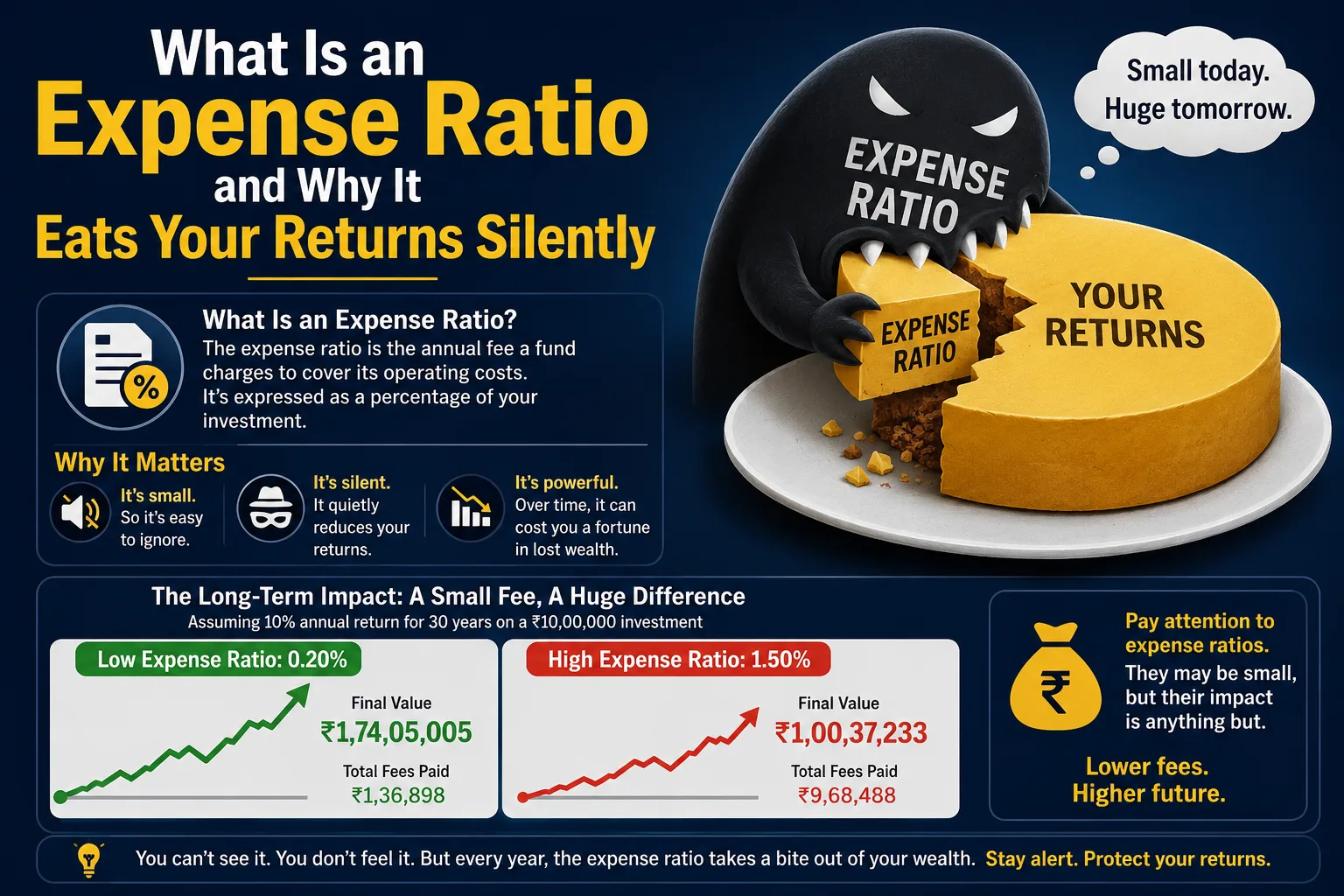

This is what expense ratios do. They work in silence. And most Indian investors have no idea they’re paying them at all.

What Exactly Is a Mutual Fund Expense Ratio?

The expense ratio is the annual fee that a mutual fund charges to manage your money. It covers the fund manager’s salary, administrative costs, marketing expenses, compliance, custodian fees, registrar charges — essentially everything it costs to run the fund.

SEBI mandates that every AMC (Asset Management Company) disclose this figure clearly. You’ll find it on AMFI’s website, on platforms like Groww or Zerodha’s Coin, and in every fund’s Scheme Information Document. But knowing where to find it and actually understanding what it does to your wealth are two different things.

Here’s how it works mechanically: if a fund has an expense ratio of 1.2% per annum, that charge is deducted daily from the fund’s Net Asset Value (NAV). You never see a line item that says “fee deducted.” The NAV you see every day is already net of this charge. This is why it feels invisible — because it is. The fund reports performance after deducting these costs, so on the surface, everything looks fine.

It only hurts you when you compare what you could have earned versus what you actually earned.

How Much Are Indian Funds Really Charging?

SEBI has set upper limits on expense ratios based on Assets Under Management (AUM), and the rules have tightened since 2018. For equity funds, the current cap starts at 2.25% for smaller AUM slabs and steps down as the fund grows. Debt funds have a lower cap. Index funds and ETFs, because they require minimal active management, typically charge anywhere between 0.05% and 0.50%.

But here’s where it gets interesting — and where most investors lose money without realising it.

Direct plans vs regular plans. This is arguably the most important concept in Indian mutual fund investing right now.

When you invest through a broker, a bank relationship manager, or a third-party distributor app, you’re buying the regular plan of a mutual fund. A portion of that expense ratio — called the trail commission — goes to the distributor as ongoing compensation, every single year you stay invested. When you invest directly through the AMC’s website or a direct platform like Zerodha Coin or Groww’s direct plan option, you buy the direct plan. No middleman, no trail commission, lower expense ratio.

The gap between direct and regular plans typically ranges from 0.5% to 1.5% per year, depending on the fund category.

The Compounding Trap: A Real Rupee Comparison

Let’s put numbers to it. Assume you invest ₹5,000 per month via SIP for 20 years. The underlying portfolio generates 12% per annum before expenses.

| Plan Type | Expense Ratio | Approx. Corpus After 20 Years |

|---|---|---|

| Direct Plan (Index Fund) | 0.20% | ₹49.2 lakh |

| Direct Plan (Active Equity Fund) | 0.80% | ₹46.4 lakh |

| Regular Plan (Active Equity Fund) | 1.80% | ₹42.1 lakh |

| Regular Plan (High-Cost Fund) | 2.25% | ₹39.6 lakh |

The difference between the lowest and highest cost option? Nearly ₹9.6 lakh — on a total investment of ₹12 lakh. That’s 80% of your principal, gone to fees.

And notice something important here: the regular plan investor isn’t getting a better service or higher returns to justify that extra cost. In most cases, SEBI data and independent analysis from platforms like Value Research and Prime Investor consistently show that regular plans underperform their direct counterparts purely because of the higher expense drag.

Why This Matters Even More for Indian Investors

Indian mutual fund investors face a cost structure that, historically, has been among the higher ones in Asia. While markets like the US have seen expense ratios collapse toward zero on index products, many Indian actively managed funds still charge 1.5–2% per annum. When you consider that Indian equity markets have delivered around 12–14% CAGR over long periods (Sensex and Nifty 50 both reflect this), a 1.5% annual drag represents roughly 10–12% of your gross return, every single year.

That’s not a rounding error. That’s real money.

There’s also a tax dimension worth understanding. Because mutual fund expense ratios are deducted at the fund level before NAV is declared, they don’t show up in your income tax filing at all — you can’t claim them as a deduction. Unlike brokerage on direct stock trades (where STT is at least visible), expense ratios are fully embedded and non-recoverable. Your LTCG tax at 12.5% (for equity gains above ₹1.25 lakh) is calculated on the already-reduced, post-expense NAV — so you pay tax on returns that have already been silently trimmed.

Common Mistakes Indian Investors Make Around Expense Ratios

Choosing a fund based on past returns without checking if those returns were from a direct or regular plan. Many comparison sites, especially older ones, mix both. Always check which plan the return figure belongs to.

Assuming a higher expense ratio means better management. Multiple studies, including data published by SEBI itself, show that fund manager alpha rarely justifies the cost differential — especially over 10+ year periods. A large-cap actively managed fund charging 1.8% needs to consistently beat a Nifty 50 index fund charging 0.2% by more than 1.6% every year, just to break even on cost. Very few do.

Ignoring expense ratios on ELSS funds because “80C deduction covers it.” Yes, ELSS gives you a ₹1.5 lakh deduction under Section 80C. But if your ELSS charges 1.9% per annum on a regular plan, you’re leaving substantial long-term corpus on the table. There are direct-plan ELSS options charging under 1%, and the tax benefit is identical.

Not reviewing expense ratios when switching platforms. Many investors start on one app and migrate later, sometimes unknowingly shifting from a direct plan back to a regular plan on a new platform. Always verify the plan type after every platform migration.

Practical Steps to Cut Your Expense Ratio Costs Starting Today

Step 1 — Audit your current holdings. Log into AMFI’s website (amfiindia.com) or check your Consolidated Account Statement (CAS) from CAMS or KFintech. For every fund you hold, note whether it’s a direct or regular plan.

Step 2 — Switch to direct plans where applicable. You can switch directly on the AMC’s website, through Zerodha Coin, Groww’s direct plan section, or MF Utility. Switching within equity funds may trigger STCG or LTCG — check the holding period before switching. For ELSS funds, remember the three-year lock-in before any switch is possible.

Step 3 — Prioritise low-cost index funds for your core portfolio. For categories like large-cap equity, Nifty 50, or Nifty Next 50 exposure, direct index funds with expense ratios under 0.30% are available from AMCs like UTI, HDFC, and Nippon. These make a compelling core allocation for most investors.

Step 4 — Use the expense ratio filter actively. On Groww and Kite/Coin, you can filter funds by expense ratio. Make it a non-negotiable part of your fund selection checklist — alongside 5-year rolling returns, fund manager track record, and AUM stability.

Step 5 — Revisit annually. SEBI allows AMCs to revise expense ratios within permissible limits. A fund you chose two years ago may now charge differently. An annual review takes 20 minutes and can be worth lakhs over time.

Key Takeaways

- The mutual fund expense ratio is an annual fee deducted daily from your NAV — invisible in statements but deeply real in its long-term impact on your wealth.

- Over 15–20 years, a 1–1.5% difference in expense ratio can erode ₹8–10 lakh on a modest SIP — more than your total invested principal in many cases.

- Direct plans consistently beat regular plans of the same fund, purely because of lower expense ratios — the underlying portfolio is identical.

- Index funds offer the lowest expense ratios in Indian markets (0.05–0.50%), making them highly cost-efficient for large-cap and broad market exposure.

- Switching from regular to direct plans may have short-term LTCG/STCG implications — plan the switch strategically, especially for older, well-performing holdings.

- Expense ratios don’t appear in your P&L, can’t be claimed as a tax deduction, and compound against you silently — which makes them one of the most underestimated wealth destroyers in Indian retail investing.

The market can’t be controlled. Your costs can. That’s the one edge every investor has, and most never use it.