Quick Answer: SIP (Systematic Investment Plan), STP (Systematic Transfer Plan), and SWP (Systematic Withdrawal Plan) are three powerful mutual fund tools that help Indian investors build wealth, manage risk, and create tax-efficient income — at different stages of their financial journey.

Introduction: Why These Three Terms Could Change Your Financial Life

Most Indian investors know SIP. Fewer know STP. And very few use SWP to its full potential.

Yet together, these three tools form a complete investment lifecycle — one that can take you from your first ₹500 monthly investment all the way to a steady, tax-efficient retirement income.

At Techolic, we’ve broken down complex financial concepts for thousands of Indian readers. This guide is built on one belief: financial clarity should be accessible to every Indian, not just those with a CA on speed dial.

Whether you’re a 25-year-old just starting out or a 55-year-old approaching retirement, understanding SIP, STP, and SWP — and how they work together — is one of the most valuable things you can do for your money.

Let’s start from the beginning.

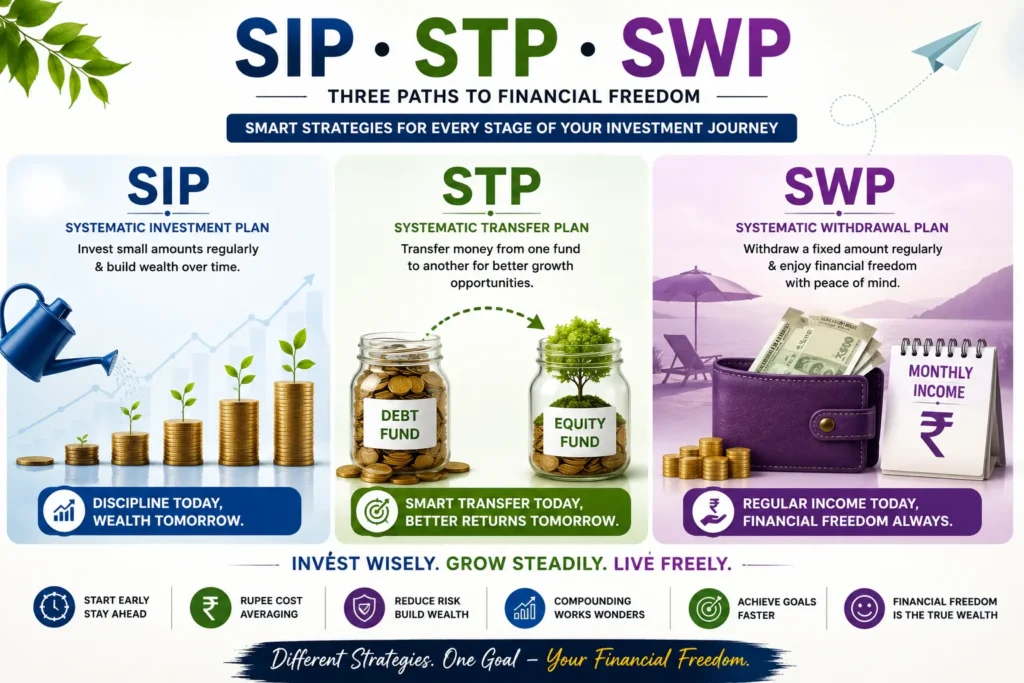

What Is SIP (Systematic Investment Plan)?

A Systematic Investment Plan (SIP) is a method of investing a fixed amount in a mutual fund scheme at regular intervals — typically monthly. Instead of investing a large lump sum, you invest small amounts consistently over time.

How SIP Works

When you start a SIP of ₹5,000/month in an equity mutual fund, your bank automatically debits ₹5,000 on a set date every month. That money buys units of the fund at the current NAV (Net Asset Value). When NAV is high, you get fewer units. When NAV is low, you get more units.

Over time, this averages out your cost of purchase — a principle called Rupee Cost Averaging.

Key Benefits of SIP for Indian Investors

- Rupee Cost Averaging: You naturally buy more units when markets fall, reducing your average cost

- Power of Compounding: Returns compound over time, especially with long holding periods (10–30 years)

- Discipline Without Willpower: Automation removes the temptation to time the market

- Low Entry Point: Start with as little as ₹100/month with most fund houses

- Flexibility: Pause, increase, or stop your SIP anytime without penalties

SIP Real-World Example

| Monthly SIP | Duration | Assumed Return | Total Invested | Estimated Corpus |

| ₹5,000 | 10 years | 12% p.a. | ₹6,00,000 | ₹11.6 lakh |

| ₹5,000 | 20 years | 12% p.a. | ₹12,00,000 | ₹49.9 lakh |

| ₹5,000 | 30 years | 12% p.a. | ₹18,00,000 | ₹1.76 crore |

Note: Returns are illustrative and not guaranteed. Equity investments are subject to market risk.

The difference between 10 years and 30 years is not 3x — it’s 15x. That’s the compounding effect.

Types of SIP

- Regular SIP – Fixed amount, fixed date, monthly

- Step-Up SIP (Top-Up SIP) – Automatically increases your investment amount by a fixed % each year

- Flexi SIP – Varies the amount based on market conditions

- Trigger SIP – Activates on specific market events (NAV level, index value)

- Perpetual SIP – No end date; continues until you stop it

Techolic Tip: A Step-Up SIP aligned with your annual salary hike is one of the most underused wealth-building tools in India. Increasing your SIP by just 10% every year can nearly double your final corpus versus a flat SIP.

What Is STP (Systematic Transfer Plan)?

A Systematic Transfer Plan (STP) allows you to automatically transfer a fixed amount from one mutual fund to another — usually from a debt fund to an equity fund — at regular intervals.

Think of STP as a SIP, but instead of investing fresh money from your bank account, you’re deploying money that’s already parked in a mutual fund.

Why Do Indian Investors Use STP?

The most common use case: You receive a lump sum — a bonus, PF withdrawal, property sale proceeds, or an inheritance — but you don’t want to dump it all into equity markets at once.

Instead, you park the entire amount in a liquid or ultra-short-term debt fund and then use STP to move it into an equity fund in monthly installments over 12–24 months.

This gives you two advantages:

- Your lump sum earns better-than-savings-account returns while it sits in the debt fund

- You gradually enter the equity market, reducing timing risk

How STP Works — Step by Step

Step 1: Invest ₹12,00,000 (lump sum) in a liquid mutual fund

Step 2: Set up an STP of ₹1,00,000/month to transfer to an equity mutual fund

Step 3: Every month, ₹1,00,000 moves from the liquid fund to the equity fund

Step 4: After 12 months, your entire corpus is invested in equity — bought at 12 different price points

STP vs SIP — Key Differences

| Feature | SIP | STP |

| Source of funds | Your bank account | Another mutual fund |

| Best for | Regular income earners | Lump sum investors |

| Idle money earns returns | No | Yes (in debt fund) |

| Market timing risk | Reduced | Reduced |

| Tax on transfers | Not applicable | Yes — each transfer is a redemption |

Tax Note on STP (Important!)

Every STP transfer is treated as a redemption from the source fund and a fresh purchase in the destination fund. This means capital gains tax applies on the debt fund withdrawals. For transfers within 3 years, Short-Term Capital Gains (STCG) tax at your income slab rate will apply on profits.

Always factor this in when calculating returns.

Types of STP

- Fixed STP – Transfer a fixed amount (e.g., ₹50,000/month)

- Capital Appreciation STP – Transfer only the profit earned in the source fund; principal stays intact

- Flexi STP – Transfer variable amounts based on market levels

Techolic Tip: Capital Appreciation STP is ideal for conservative investors. Your original corpus stays safe in a debt fund while only the gains get invested in equity — a near-zero-risk equity exposure strategy.

What Is SWP (Systematic Withdrawal Plan)?

A Systematic Withdrawal Plan (SWP) is the opposite of a SIP. Instead of putting money in at regular intervals, you take money out at regular intervals.

SWP allows you to redeem a fixed amount from your mutual fund at a set frequency — monthly, quarterly, or annually — directly to your bank account.

Who Should Use SWP?

SWP is most powerful for:

- Retirees who need monthly income from their corpus

- Anyone who has reached their goal and wants to start using that money

- Investors who want passive income without selling their entire investment

Why SWP Is Better Than Dividend Option

Many Indian investors choose the Dividend Plan of a mutual fund for regular income. SWP is almost always the smarter choice.

| Feature | Dividend Plan | SWP |

| Tax | Dividend added to income, taxed at slab rate (up to 30%) | Only capital gains taxed — often at lower rates |

| Control | Fund decides dividend amount and timing | You decide amount and date |

| Principal | Erodes with each dividend | Can remain intact if returns > withdrawal |

| Predictability | Inconsistent — depends on fund performance | Fixed, predictable monthly income |

SWP Tax Advantage — A Real Example

Suppose you have ₹50 lakh in an equity mutual fund and withdraw ₹25,000/month via SWP.

Each ₹25,000 withdrawal has two components:

- Return of principal (not taxable)

- Capital gain (a small portion of each withdrawal)

If the fund was held for over 1 year, only the capital gain portion is taxed at 10% (LTCG above ₹1 lakh/year). The principal portion? Zero tax.

Compare this to a fixed deposit: the entire interest income is taxed at your slab rate (up to 30%). SWP can save you lakhs in tax over a retirement period of 20+ years.

SWP Real-World Example

Corpus: ₹1 crore invested in a balanced mutual fund SWP Amount: ₹40,000/month Assumed Return: 10% p.a.

At this rate, your corpus doesn’t just survive — it grows. You withdraw ₹4.8 lakh a year while the fund potentially earns ₹10 lakh in returns. Your principal continues to appreciate.

Note: Returns are not guaranteed. Past performance is not indicative of future results.

SIP + STP + SWP: The Complete Investment Lifecycle

Here’s the key insight most investors miss — these three tools are not separate products. They are three chapters of the same story.

The Three Stages of a Smart Indian Investor’s Journey

ACCUMULATION PHASE TRANSITION PHASE DISTRIBUTION PHASE

(Age 25–50) (Age 50–60) (Age 60+)

SIP STP SWP

─── ─── ───

Invest monthly Move equity corpus to Withdraw monthly

from salary debt/balanced funds as retirement income

Build corpus Reduce market risk Tax-efficiently

Stage 1 — Build (SIP): Invest ₹10,000–₹50,000/month over 20–30 years in equity mutual funds. Let compounding work.

Stage 2 — Protect (STP): As retirement approaches, use STP to gradually shift your equity corpus into debt/hybrid funds. Reduce your market exposure without exiting in one go.

Stage 3 — Withdraw (SWP): Once retired, use SWP to draw a monthly “salary” from your corpus — tax-efficiently, predictably, and sustainably.

Common Mistakes Indian Investors Make

Mistake 1: Stopping SIP During Market Corrections

Market dips are exactly when SIP works best. You buy more units at lower prices. Stopping a SIP during a correction locks in losses and destroys the rupee cost averaging benefit.

Mistake 2: Using SWP Without Keeping Enough in Equity

If your entire corpus is in a debt fund and you run SWP, you may eat into principal. Keep some equity allocation to let returns fund your withdrawals.

Mistake 3: Ignoring Tax on STP Transfers

Each STP redemption from the source fund is taxable. For short tenures (under 3 years in debt funds), this eats into your returns. Plan accordingly.

Mistake 4: Not Using Step-Up SIP

Inflation grows at ~6% per year. A flat SIP gradually loses purchasing power. Step-up your SIP annually in line with salary hikes.

Mistake 5: Choosing Dividend Plan Instead of Growth + SWP

As shown above, the tax inefficiency of dividend plans versus a Growth plan with SWP is significant — especially for high-income earners.

Frequently Asked Questions (FAQ)

Q: Can I run SIP and SWP from the same mutual fund at the same time?

Yes, technically possible, but not recommended. It creates unnecessary complexity and tax events. Ideally, SIP and SWP should be at different life stages.

Q: What is the minimum amount for STP in India?

Most fund houses require a minimum of ₹500–₹1,000 per STP instalment. The source fund typically requires a minimum balance of ₹12,000–₹25,000 depending on the AMC.

Q: Is SWP income considered salary? Is it taxable?

SWP is not salary income. It is a redemption from a mutual fund. Only the capital gain component is taxable — either as STCG or LTCG depending on the holding period. The principal return is not taxed.

Q: How many SIPs can I run simultaneously?

There is no legal limit. You can run multiple SIPs across different fund houses and schemes. Most investors run 3–5 SIPs across large-cap, mid-cap, flexi-cap, and ELSS funds.

Q: What happens to my SIP if the fund house shuts down?

SEBI (Securities and Exchange Board of India) regulations ensure your money is held in a trust separate from the AMC’s own finances. If an AMC shuts down, SEBI appoints a new manager or facilitates a merger. Your money is protected.

Q: Can I do STP from equity to debt?

Yes. This is called a Reverse STP and is commonly used as retirement approaches — gradually shifting equity gains to the safety of debt funds.

Q: What is a better option — SWP or pension plan (annuity)?

SWP typically offers better flexibility, liquidity, and tax efficiency versus traditional annuity products. However, annuities offer guaranteed income for life, which SWP cannot promise since it depends on market performance. Most financial planners recommend a combination of both.

Expert Insight: What Financial Advisors in India Recommend

Certified Financial Planners (CFPs) in India consistently recommend the following SIP-STP-SWP framework for salaried professionals:

- Start SIP early — even ₹2,000/month at age 22 beats ₹20,000/month at age 40 in long-term corpus building

- Step-up every April — align your SIP hike with your annual appraisal month

- Begin STP 5–7 years before retirement — don’t wait until the last year to de-risk

- Set SWP at 3–4% of corpus per year — this is the “safe withdrawal rate” in Indian market conditions, accounting for inflation and market volatility

- Review annually — asset allocation and withdrawal rates must be reviewed as markets and life circumstances change

Summary: SIP vs STP vs SWP at a Glance

| SIP | STP | SWP | |

| Full form | Systematic Investment Plan | Systematic Transfer Plan | Systematic Withdrawal Plan |

| Direction | Bank → Mutual Fund | Fund → Fund | Mutual Fund → Bank |

| Primary goal | Build wealth | Manage transition risk | Generate income |

| Best suited for | Working professionals | Lump sum investors / Pre-retirees | Retirees / Goal achievers |

| Tax event | No (investing fresh money) | Yes (redemption from source fund) | Yes (capital gains on redemption) |

| Key benefit | Rupee cost averaging | Safe lump sum deployment | Tax-efficient regular income |

Final Word from Techolic

SIP, STP, and SWP are not three separate products you choose between — they are three tools in one toolkit, each serving a different phase of your financial life.

The most successful Indian investors we’ve studied aren’t necessarily those who picked the “best fund.” They’re the ones who stayed invested through corrections (SIP), de-risked intelligently before retirement (STP), and created a sustainable income stream that lasted decades (SWP).

Financial literacy is not a luxury. At Techolic, we believe it’s a right — and knowing how these three tools work together is one of the most empowering pieces of knowledge any Indian investor can have.

Start your SIP today. Plan your STP decade in advance. Structure your SWP to retire with dignity.