With easy access to trading apps, market data, and financial content, many investors today ask a valid question:

Should I manage my investments on my own, or should I work with a professional financial advisor?

Both DIY investing and professional advisory services have their place. The right choice depends on your experience, time availability, financial goals, and risk tolerance.

This article breaks down both approaches clearly, helping you decide what works best for your situation.

What Is DIY Investing?

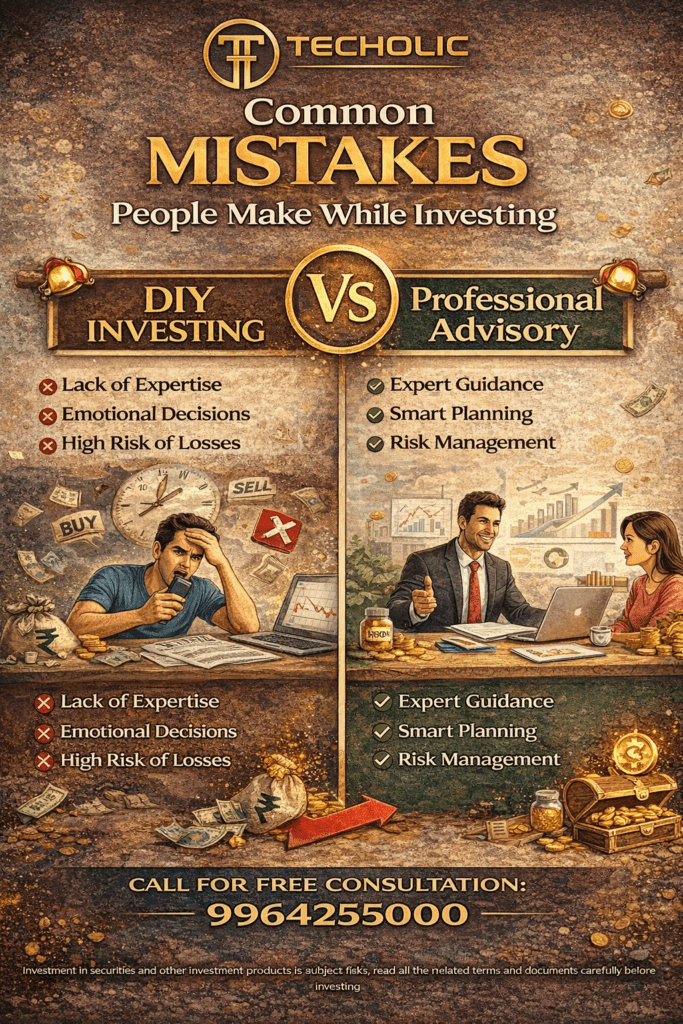

DIY (Do-It-Yourself) investing means making all investment decisions independently. You choose the stocks, mutual funds, or other instruments, execute trades yourself, and manage your portfolio without professional guidance.

Common Reasons Investors Choose DIY Investing

- Lower advisory costs

- Full control over decisions

- Interest in market research

- Hands-on learning approach

DIY investing is popular among active traders and market-savvy investors, but it comes with responsibilities.

What Is Professional Advisory?

Professional advisory involves working with a qualified financial advisor or stock broker who provides guidance based on your financial profile.

A professional advisor helps with:

- Portfolio construction

- Risk assessment

- Market strategy

- Ongoing review and rebalancing

This approach focuses on structured, goal-oriented investing rather than isolated trades.

Key Differences: DIY Investing vs Professional Advisory

1. Decision-Making Responsibility

DIY Investing:

You are fully responsible for:

- Research

- Entry and exit timing

- Risk management

- Emotional discipline

Professional Advisory:

Decisions are:

- Data-driven

- Aligned with your goals

- Supported by market experience

👉 Ask yourself:

Do I have the time and confidence to make consistent investment decisions?

2. Risk Management Approach

DIY Investing Risks:

- Over-trading

- Poor diversification

- Emotional reactions during volatility

Professional Advisory Benefits:

- Risk-adjusted strategies

- Portfolio diversification

- Downside protection focus

Professional advisors aim to protect capital first, then grow it.

3. Time Commitment

DIY investing requires:

- Daily or weekly market tracking

- Continuous learning

- Regular portfolio reviews

Professional advisory saves time by:

- Handling analysis

- Monitoring market changes

- Providing timely recommendations

👉 Consider:

Can I consistently dedicate time to manage my investments properly?

4. Emotional Control During Market Volatility

Markets test emotions.

DIY Investors often struggle with:

- Panic selling during corrections

- Greed during rallies

- Frequent strategy changes

Professional advisors help by:

- Providing objective guidance

- Preventing impulsive decisions

- Maintaining long-term discipline

This emotional support alone can significantly impact long-term returns.

Cost vs Value: Is Professional Advisory Worth It?

Many investors focus only on advisory fees, ignoring the value delivered.

DIY Investing Costs (Hidden)

- Poor entry/exit decisions

- Concentrated positions

- Missed opportunities

- Losses due to emotional trading

Professional Advisory Value

- Structured portfolio strategy

- Consistent risk monitoring

- Goal-based investing

- Accountability and clarity

The right advisor often prevents costly mistakes, which outweigh advisory fees over time.

Who Should Choose DIY Investing?

DIY investing may suit you if:

- You have strong market knowledge

- You actively track markets

- You understand risk management

- You are comfortable with volatility

DIY works best for experienced investors who treat investing like a discipline, not a hobby.

Who Should Choose Professional Advisory?

Professional advisory is ideal if:

- You want goal-based investing

- You prefer structured planning

- You lack time or expertise

- You want risk-controlled growth

It is especially beneficial for:

- Long-term investors

- Business owners

- High Net Worth Individuals (HNIs)

- First-time or cautious investors

Frequently Asked Investor Questions

❓ Is DIY investing cheaper than professional advisory?

DIY may appear cheaper, but mistakes can be costly. Professional advisory focuses on long-term value, not short-term savings.

❓ Can I mix DIY investing with professional advisory?

Yes. Many investors:

- DIY a portion of their portfolio

- Use advisors for core investments

This hybrid approach offers flexibility with discipline.

❓ Does professional advisory guarantee returns?

No ethical advisor guarantees returns. The focus is on risk management, consistency, and long-term wealth creation.

❓ How do I know if I need a financial advisor?

If you are unsure about:

- Asset allocation

- Market cycles

- Portfolio risk

- Long-term strategy

Then professional advisory can add significant value.

Final Verdict: Which Is Better for You?

There is no universal answer.

DIY investing offers control and cost savings — but demands time, skill, and emotional discipline.

Professional advisory offers structure, clarity, and risk management — helping investors stay aligned with their goals across market cycles.

The best choice depends on your financial complexity and expectations.

Take the Next Step with Confidence

If you want:

- Personalized investment strategies

- Risk-managed portfolio planning

- Professional guidance aligned with your goals

Working with a trusted financial advisor or stock broker can help you make more informed, confident investment decisions.

Because successful investing is not about doing more — it’s about doing it right.