Every IPO season, the same pattern repeats itself across India. Investors check the Grey Market Premium, ask around in WhatsApp groups, read a two-line summary on a financial news app, and apply. The stock lists. Sometimes they gain, sometimes they don’t — and in most cases, they have no real idea why.

The Draft Red Herring Prospectus — the DRHP — exists precisely to prevent that. It is the single most comprehensive document a company is legally required to file before going public. It tells you what the business actually does, where the IPO money is going, what risks the company itself acknowledges, who the promoters are, and whether there are any ongoing legal disputes that could affect the company post-listing.

Most retail investors never open it. Those who do rarely know which sections matter and which ones they can skim past. This guide fixes that — and with two of India’s most anticipated IPOs, the NSE and Jio Platforms, having filed their DRHPs in June 2026, there has never been a better time to learn how to read one.

What Is a DRHP and Why Does SEBI Mandate It?

The DRHP — Draft Red Herring Prospectus — is the preliminary document filed by a company with SEBI (Securities and Exchange Board of India) before launching an IPO. It is mandatory for every mainboard IPO in India, governed under SEBI’s Issue of Capital and Disclosure Requirements (ICDR) Regulations, 2018.

The word “draft” is deliberate. It signals that the document is not yet final — the IPO price band and lot size are not yet determined when the DRHP is filed. Those details appear only in the Red Herring Prospectus (RHP), which is filed closer to the IPO opening date.

Once the DRHP is filed with SEBI, it must remain publicly available for a minimum of 21 days — anyone can download and read it from SEBI’s website, BSE/NSE websites, or the lead merchant banker’s website. SEBI typically issues its observation letter within 30 days, though complex filings can take longer. The NSE DRHP, filed on June 17, 2026 for a ₹30,000 crore issue, is currently in exactly this review stage — a live example of how this process unfolds in real time.

The DRHP is a legally binding document. Every director signs it and carries personal legal liability for its accuracy. Any material misstatement or omission can attract SEBI penalties and civil liability. That level of accountability is exactly why it is the most reliable document available to you before an IPO.

DRHP vs RHP: What’s the Difference?

These two documents confuse a lot of first-time investors. Here’s how they differ:

The DRHP is the draft filed with SEBI for review. It contains all material disclosures about the company but does not include the final price band or IPO dates. It is the document you read for research — before you decide whether to even consider applying.

The RHP is filed with the Registrar of Companies just before the IPO subscription window opens. It includes the final price band, the IPO opening and closing dates, and all final disclosures. This is the document on which you make your actual application.

The practical takeaway: Read the DRHP well before the IPO opens. Most investors only discover the RHP during the 3-day subscription window, which is far too little time to analyse a 300–400 page document carefully.

Where to Download the DRHP

You don’t need a broker, a subscription, or special access. The DRHP is a public document:

- SEBI’s official website — sebi.gov.in (under the Primary Market section)

- NSE and BSE websites — both maintain dedicated IPO sections with all filed DRHPs

- The lead merchant banker’s website — named clearly in every DRHP

- The company’s own website — typically under Investor Relations

Download the PDF directly. Do not rely on third-party summaries for investment decisions — they compress or omit the exact sections that matter most.

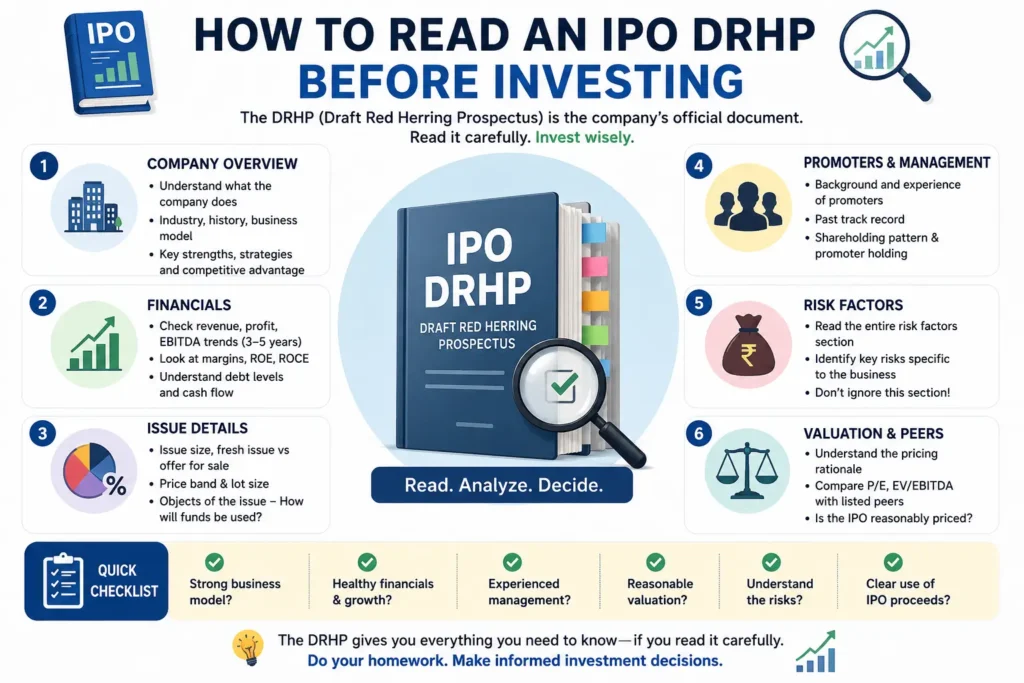

How to Read a DRHP: The Sections That Actually Matter

A typical DRHP runs between 300 and 500 pages. You don’t need to read every word of every section. Here is a prioritised approach — what to read first, what to read carefully, and what you can skim.

Section 1: Objects of the Issue — Where Is Your Money Actually Going?

This is the first section every investor should read, and the NSE vs Jio contrast makes it more relevant than ever right now.

There are two types of IPO structures, and their distinction matters enormously:

Fresh Issue: New shares are created and sold. The money raised flows directly into the company — for expansion, debt repayment, working capital, or technology investment. A fresh issue means the IPO is genuinely about funding the business.

Offer for Sale (OFS): Existing shareholders — promoters, private equity investors, early backers — sell part of their stake to the public. The money goes entirely to the sellers, not the company. The company receives nothing from an OFS.

Two of India’s most closely watched IPOs, both filed within days of each other in June 2026, illustrate this perfectly:

NSE IPO (DRHP filed June 17, 2026): Structured as a 100% OFS of approximately 14.89 crore shares, targeting ₹30,000 crore. The exchange itself receives zero fresh capital. Existing shareholders — SBI, LIC, Canada Pension Plan Investment Board, and others — are selling their stakes. NSE is a profitable, institutionally sound business, so this isn’t a red flag about the company’s health. But it is critical context: you are buying a stake from sellers who are exiting, not funding a growth story.

Jio Platforms IPO (DRHP filed June 19, 2026): Structured as a 100% Fresh Issue of up to 27 crore equity shares, with an estimated size of ~₹37,700 crore. Every rupee raised goes directly into Jio Platforms — ₹27,500 crore earmarked specifically for debt repayment at its subsidiary Reliance Jio Infocomm Limited (RJIL), with the balance for general corporate purposes including AI infrastructure and network expansion. This is a textbook growth-capital raise.

Same month, two landmark IPOs, two completely opposite structures. One question — “where does my money go?” — gives you the most important piece of context in 60 seconds.

Green flag: Fresh issue proceeds allocated to specific, costed projects — capacity, debt reduction, technology.

Red flag: IPO that is 80–90% OFS with minimal fresh issue, or proceeds earmarked to “general corporate purposes” without specific breakdowns.

Section 2: Risk Factors — The Section Nobody Reads But Should

This section is arguably the most important in the entire document. Companies are legally required by SEBI to disclose all material risks, listed roughly in order of severity — the most significant ones appear first.

This is where companies tell you, in their own words, what could go wrong. The NSE’s DRHP, for instance, discloses risks around historical regulatory enforcement actions related to its co-location controversy, dependence on market trading volumes, intense competition from BSE in certain segments, and the absence of identifiable promoters — an unusual structure for a systemically important institution. None of this makes NSE a bad investment, but each point is something an informed investor should weigh.

What to specifically look for in any DRHP:

- Customer concentration: If more than 30% of revenue comes from a single client, losing that relationship could devastate the business

- Litigation involving promoters: Ongoing court cases, SEBI show-cause notices, or income tax investigations mentioned here deserve serious attention

- Regulatory dependency: If the business depends on government licences, approvals, or contracts that could be revoked, that is a structural risk

- Key person dependency: If the entire operation depends on one or two individuals, what happens if they leave?

- Related party transactions: Deals between the company and promoter-linked entities at potentially non-market prices

A useful rule: read the wording of each risk factor carefully, not just the headline. Companies are sometimes incentivised to bury critical risks inside legally compliant but practically obscure language. The information is there — you just have to look.

Section 3: Financial Statements — What the Numbers Actually Tell You

The DRHP includes audited financial statements for at least the last three years — income statements, balance sheets, and cash flow statements. This is where you assess whether the company is genuinely healthy or has been dressed up for listing.

Jio Platforms’ DRHP, for instance, discloses strong FY26 financials: revenue from operations of ₹1,46,885 crore (up 14.6% year-on-year), net profit of ₹30,049 crore (up 15.1%), and EBITDA margins expanding to 51.9%. Consistent multi-year growth like this, visible in the financials section, is exactly the kind of signal you look for. The NSE DRHP, by contrast, shows a 3.1% revenue decline and a 15.5% drop in PAT for FY26 — not alarming for a mature exchange business, but the kind of detail that shapes your valuation thinking.

What to check in any DRHP:

- Revenue growth consistency: Is it steady over 3–5 years, or is there a sudden spike only in the year before IPO filing?

- Profitability: Is the company profitable, or burning cash with no clear path to profitability?

- Cash flow from operations: Consistent positive operating cash flow is a stronger signal than reported profit alone

- Debt levels: High debt with thin margins is a structural concern. Also check whether significant borrowing happened in the six months before the DRHP filing

- Notes to accounts: Aggressive revenue recognition policies, unusual depreciation methods, or large off-balance-sheet items all show up here — read them

Red flag: A dramatic revenue or profit jump only in the year immediately before IPO filing — a possible sign of window-dressing.

Section 4: Promoter and Management Background

The promoters section tells you who owns and controls the company — their professional background, shareholding patterns before and after the IPO, whether they have pledged shares as collateral, and any criminal cases or regulatory actions against them.

For Jio Platforms, the DRHP discloses that Reliance Industries holds 66.43% — a significant majority stake being retained post-IPO. Global investors Meta and Google are also among key shareholders. Promoter confidence is visible in the fact that no existing shareholder is using the IPO to exit — the entire issue is fresh capital. For NSE, given the absence of a traditional promoter group, the selling shareholders section becomes the equivalent analysis — understanding who is selling, how much, and why.

What to look for in any DRHP:

- Post-IPO promoter holding: Above 60% generally signals confidence. Below 40% warrants checking whether a large OFS is driving the reduction

- Pledged shares: If promoters have pledged a large percentage as collateral, forced selling during a price fall can create additional downward pressure

- Track record with past ventures: The DRHP discloses other companies associated with the promoter group

- Related party transactions: Consulting fees to promoter-linked entities or asset purchases from promoter-controlled companies without clear justification are warning signs

Section 5: Legal and Regulatory Proceedings

All pending court cases — criminal, civil, and regulatory — are disclosed here. One or two minor cases are normal for any large business. Multiple regulatory actions, income tax disputes for material amounts, or customer fraud cases are a different matter.

NSE’s DRHP is instructive here. It discloses the decade-long co-location controversy, the ₹1,387 crore settlement with SEBI, and other regulatory matters — all now substantially resolved before the filing. This is how transparent disclosure is supposed to work: the company flags the history, explains the resolution, and lets investors judge the residual risk. Pay special attention when litigation involves the promoters personally rather than just the company, as this creates governance uncertainty that can persist post-listing.

Red Flags to Watch in Any DRHP

- IPO is 70–100% OFS with minimal fresh issue — insiders are primarily exiting

- Revenue or profit spikes dramatically only in the year before IPO filing

- Customer concentration above 30% from a single client

- Promoters have pledged a significant percentage of their shares

- Risk factors mention SEBI investigations, show-cause notices, or material tax disputes

- Large recurring related-party transactions with no clear justification

- Significant new borrowing in the 6 months before DRHP filing

- Proceeds allocated to “general corporate purposes” without specific breakdowns

The Mistake Most Indian IPO Investors Make

Applying based on GMP (Grey Market Premium) alone. Even for the NSE IPO — one of the most anticipated listings in a decade — the GMP is unregulated, informal, and driven purely by market sentiment. It is not a SEBI-recognised indicator of anything. For the Jio Platforms IPO, no active GMP even exists yet since the price band has not been announced.

The DRHP is what separates informed investors from those gambling on listing day buzz. At Techolic, we encourage every client to read at least the five key sections of any DRHP before applying — and we help decode what the disclosures actually mean for your portfolio. If you’re evaluating whether the NSE or Jio Platforms IPO fits your investment goals, speaking with our team before the subscription window opens is time well spent.

FAQ

Q: Is reading the DRHP mandatory before applying for an IPO?

Legally, no. Practically, it is the single most important step you can take before committing money — it is the only document where the company is required to disclose every material fact, including everything that could go wrong.

Q: Where can I access a company’s DRHP in India?

Directly from SEBI’s website (sebi.gov.in), the NSE/BSE websites, the lead merchant banker’s site, or the company’s own investor relations page. It is a free, public document. The NSE and Jio Platforms DRHPs filed in June 2026 are both publicly available there right now.

Q: How is the DRHP different from the RHP?

The DRHP is the preliminary draft filed with SEBI for review — it does not contain the final price band or IPO dates. The RHP is the finalised document released just before the subscription window opens and includes all final pricing information.

Q: Is the NSE IPO a good investment because of its brand?

Brand recognition is not a substitute for reading the DRHP. The NSE IPO being 100% OFS means you should evaluate it differently from a fresh-issue IPO — you’re buying from sellers, not funding growth. Final valuation, market conditions, and your own financial goals should drive the decision, not the name.

Q: How is the Jio Platforms IPO different from the NSE IPO in structure?

They are near-complete opposites. NSE is a 100% OFS — existing shareholders are selling, and the company receives no capital. Jio Platforms is a 100% Fresh Issue — all proceeds go into the business, with ₹27,500 crore earmarked for debt repayment. Understanding this distinction from the DRHP is exactly what separates informed IPO investors from those who apply on hype alone.

Q: Do I need to read all 400 pages of a DRHP?

No. Prioritise: Objects of the Issue, Risk Factors, Financial Statements (with notes to accounts), Promoter Background, and Legal Proceedings. These five sections give you 90% of what you need to make an informed decision.