Most investors discover the exit load and expense ratio on their mutual fund only when the redemption amount in their bank account doesn’t match what they expected. They check the NAV, multiply it by their units, and the math still doesn’t add up. That gap is usually one of two charges quietly working in the background – and almost nobody reads about them until money is already gone.

If you’ve ever pulled money out of a fund within a year of investing and received slightly less than calculated, or wondered why two similar-looking funds gave you different returns over five years despite tracking the same market, you’ve already met exit load and expense ratio. You just didn’t know their names.

This article breaks down exactly when each charge applies, how it’s calculated, and how to avoid losing money to a fee you didn’t know existed.

What Is Exit Load in a Mutual Fund?

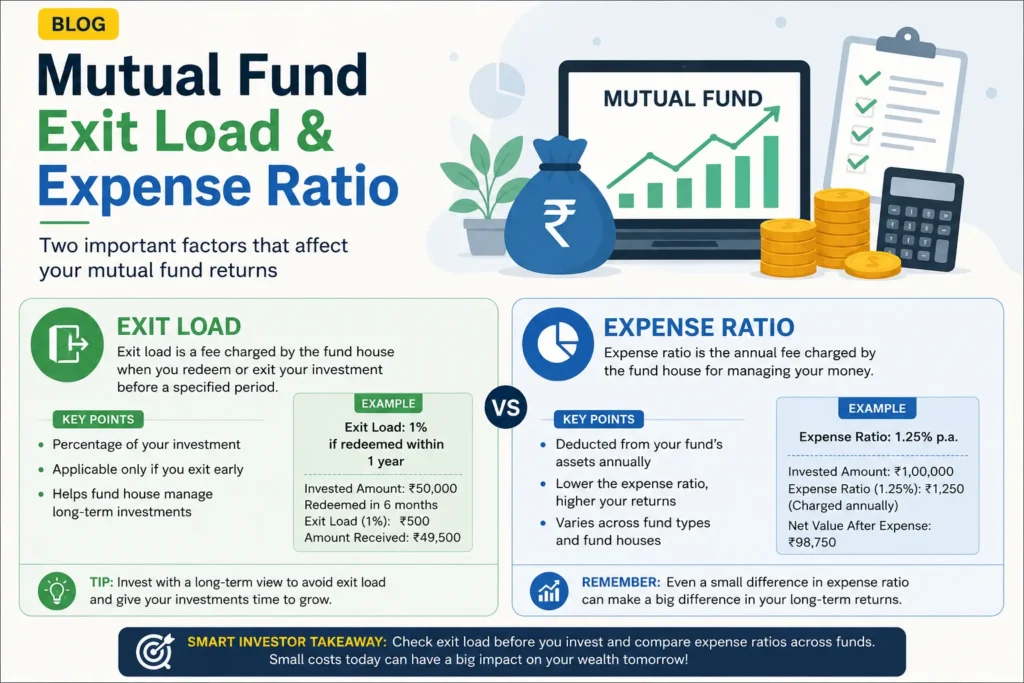

Exit load is a fee that a fund house charges when you redeem your mutual fund units before a specified holding period. It’s deducted directly from your redemption amount — you never see it as a separate transaction, you simply receive less than the NAV calculation suggested.

Think of it as a short-term exit fee, not a punishment. Fund managers build portfolios with a specific time horizon in mind. When investors pull money out too early, it forces the manager to sell holdings at potentially inconvenient times, which affects everyone else still invested in the scheme. Exit load discourages that behavior.

Here’s the part most people get wrong: exit load is not kept by the fund house as profit. It’s credited back into the scheme itself, which means it indirectly benefits the investors who stayed invested.

How Is Exit Load Calculated?

The formula is simple:

Exit Load = Exit Load Percentage × Redemption Value

Notice it’s calculated on the redemption value, not your original investment. If your fund has grown, the exit load amount grows with it.

Example: You invest ₹1,00,000 in an equity fund. After 8 months, your investment has grown to ₹1,10,000, and you decide to redeem the entire amount. The fund charges a 1% exit load for redemption within one year.

Exit load = 1% × ₹1,10,000 = ₹1,100

Amount you actually receive = ₹1,10,000 − ₹1,100 = ₹1,08,900

Wait two more months, cross the one-year mark, and you’d have received the full ₹1,10,000. That ₹1,100 difference is the exact cost of impatience.

When Does Exit Load Actually Apply?

This is where most of the confusion – and most of the lost money – happens. Exit load isn’t a flat rule across all mutual funds. It depends on the fund category and the specific holding period mentioned in the scheme document.

-

- Equity mutual funds: Most charge a 1% exit load if you redeem within 1 year. After that, it drops to zero.

- Debt mutual funds: Exit load periods are usually shorter, often a few months, and vary significantly between schemes.

- Liquid and overnight funds: SEBI mandates a graded exit load only for redemptions within 7 days, applied on a sliding scale. After 7 days, there’s no exit load at all.

- ELSS funds: No exit load applies here – but ELSS comes with a mandatory 3-year lock-in, so early redemption isn’t even possible regardless of fee.

- Some funds use tiered structures, such as 2% if redeemed within 6 months, 1% between 6–12 months, and zero after that.

SEBI currently caps the maximum exit load any mutual fund scheme can charge at 3% of the redemption value — this was reduced from the earlier 5% ceiling, specifically to prevent fund houses from using exit loads as an excessive penalty rather than a genuine discipline tool.

Does Exit Load Apply to SIPs Too?

Yes — and this is the single biggest misunderstanding among SIP investors. Many assume that once their SIP crosses a year overall, they’re free of exit load entirely. That’s incorrect.

Every SIP instalment is treated as a separate investment with its own exit load clock starting from its own date.

Example: You started a monthly SIP in July 2025. By July 2026, your SIP is technically “one year old.” But if you redeem the entire investment in July 2026, only the July 2025 instalment has crossed the one-year exit load window. The August 2025 to June 2026 instalments are all still within their individual one-year periods and will attract exit load.

If you’re planning a full redemption, check the purchase date of each instalment rather than assuming the SIP’s start date applies to everything.

Switching Between Funds Also Triggers Exit Load

Many investors believe switching from one scheme to another within the same fund house is somehow exempt from exit load. It isn’t. A switch is processed internally as a redemption from Fund A followed by a fresh purchase into Fund B. If Fund A is still within its exit load window, the charge applies — even though no money left the AMC.

How to Avoid Paying Exit Load

-

- Check the scheme’s exit load structure before investing, not at the time of redemption. It’s clearly disclosed in the scheme information document.

- Hold beyond the exit load period. This is the simplest and most reliable approach.

- Use a Systematic Transfer Plan (STP) instead of a lump-sum redemption-and-reinvest if you’re moving money between schemes gradually.

- Track installment-wise exit load dates for SIPs rather than going by the overall SIP start date.

- Redeem older instalments first when doing a partial withdrawal from a SIP, since those are more likely to be outside the exit load window.

What Is Expense Ratio in a Mutual Fund?

While exit load is a one-time charge that applies only if you exit early, the expense ratio is a recurring annual fee that applies every single year you stay invested — regardless of whether the fund makes money for you or not.

The expense ratio covers the fund house’s operating costs: fund management fees, administrative expenses, marketing, and distributor commissions (in the case of regular plans). It’s expressed as a percentage of your investment and is deducted daily from the fund’s NAV — which is why you never see it as a line item. It’s already baked into the returns you see.

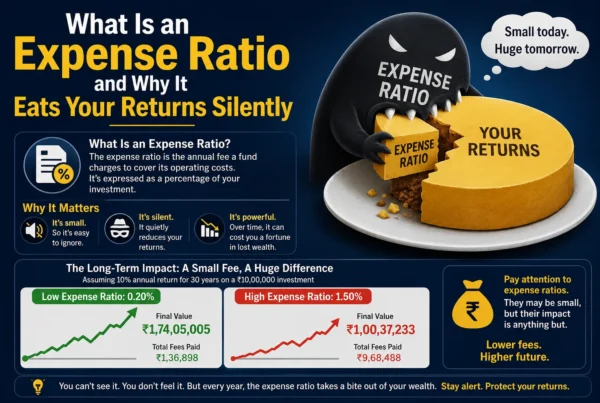

Why Expense Ratio Matters More Than People Realize

A 1% difference in expense ratio sounds negligible on paper, but compounded over 15–20 years, it can quietly eat a significant chunk of your final corpus. This is the cost most investors underestimate, simply because it’s invisible — there’s no deduction notification, no redemption slip showing the charge. It just shows up as a slightly lower return than the fund’s actual portfolio performance.

This is exactly why regular plans (which include distributor commission within the expense ratio) tend to underperform direct plans of the same scheme over long periods, even though both invest in the identical portfolio.

What’s the Current Cap on Expense Ratio?

SEBI regulates the maximum expense ratio that fund houses can charge, and this cap varies by fund category and asset size — larger funds get progressively lower permissible limits, since costs don’t scale linearly with AUM.

As part of SEBI’s broader 2026 cost-transparency overhaul, the expense ratio structure itself has become more granular. Total costs are now split into the Base Expense Ratio (BER) — the fee the fund house actually charges — and separate disclosures for brokerage, GST, STT, and other statutory charges. This split makes it easier for investors to see exactly what they’re paying the fund house for, versus what’s an unavoidable government levy.

Exit Load vs Expense Ratio: The Key Difference

It’s easy to mix these two up since both reduce your final returns, but they work very differently:

-

- Exit load applies only once, only if you redeem early, and only for a limited window of time.

- Expense ratio applies every year, automatically, regardless of when you redeem or how the fund performs.

- Exit load is a behavioral deterrent; expense ratio is an operating cost.

- You can completely avoid exit load by holding longer. You cannot avoid expense ratio — you can only minimize it by choosing a lower-cost fund or plan type.

Common Mistakes Investors Make

-

- Assuming SIP instalments share one exit load timeline instead of individual ones

- Redeeming or switching funds without checking the scheme document first

- Ignoring expense ratio differences between similar funds because the percentage gap “looks small”

- Believing exit load is a penalty that benefits the fund house, when it’s actually credited back to the scheme

- Not realizing that a switch between schemes is technically a redemption for exit load purposes

Frequently asked questions

Is exit load the same as an exit fee charged by the government?

No. Exit load is charged by the fund house (and credited back into the scheme), while taxes like capital gains tax are paid separately to the Income Tax Department on your profit.

Can a mutual fund change its exit load after I've already invested?

Yes, but any change applies prospectively from the date of the change and must be disclosed in advance — it cannot be applied retroactively to your existing investment.

Do index funds charge exit load?

Many index funds have zero exit load since they’re designed for long-term, low-cost investing, but this varies by scheme — always verify in the specific fund’s documents.

Which is more important to check before investing — exit load or expense ratio?

Expense ratio matters more for your long-term returns since it applies every year you stay invested. Exit load only matters if there’s a real chance you’ll need to exit early.

Where can I check the exact exit load and expense ratio of a fund?

Both are disclosed in the Scheme Information Document (SID) and on the AMC’s website, and are also visible on AMFI’s official portal.

Need Help?

If you're unsure how these charges are affecting your existing mutual fund portfolio, or want a clearer picture of what you're actually paying versus what you're earning, our team at Techolic can walk you through it — no jargon, just a clear breakdown of your numbers.

Contact Now