“How much harder is it, really, to retire at 40 instead of 60?” Most people guess “twice as hard” or “three times as hard.” The actual answer isn’t about a bigger number — it’s about a completely different relationship with time, and it tends to surprise even people who consider themselves financially disciplined.

This is one of the most common questions we get at Techolic, especially from professionals in their late 20s and early 30s who’ve started earning well and are wondering if early retirement is actually realistic, or just an Instagram fantasy sold by FIRE (Financial Independence, Retire Early) influencers.

The honest answer is: retiring at 40 is achievable, but it demands a completely different relationship with money than retiring at 60. It’s not just about saving more — it’s about saving earlier, investing more aggressively, and planning for a retirement that could last 40-50 years instead of 20-25.

Let’s break down the real math, the real trade-offs, and what an actual investment strategy for early retirement looks like in the Indian context.

Why Retiring at 40 Is a Completely Different Problem Than Retiring at 60

Most retirement planning advice in India is built around the 60-year retirement age, because that’s when EPF, gratuity, and most pension structures are designed to pay out. When you shift your target to 40, you’re not just moving the goalpost — you’re changing the entire game.

Here’s what changes:

-

-

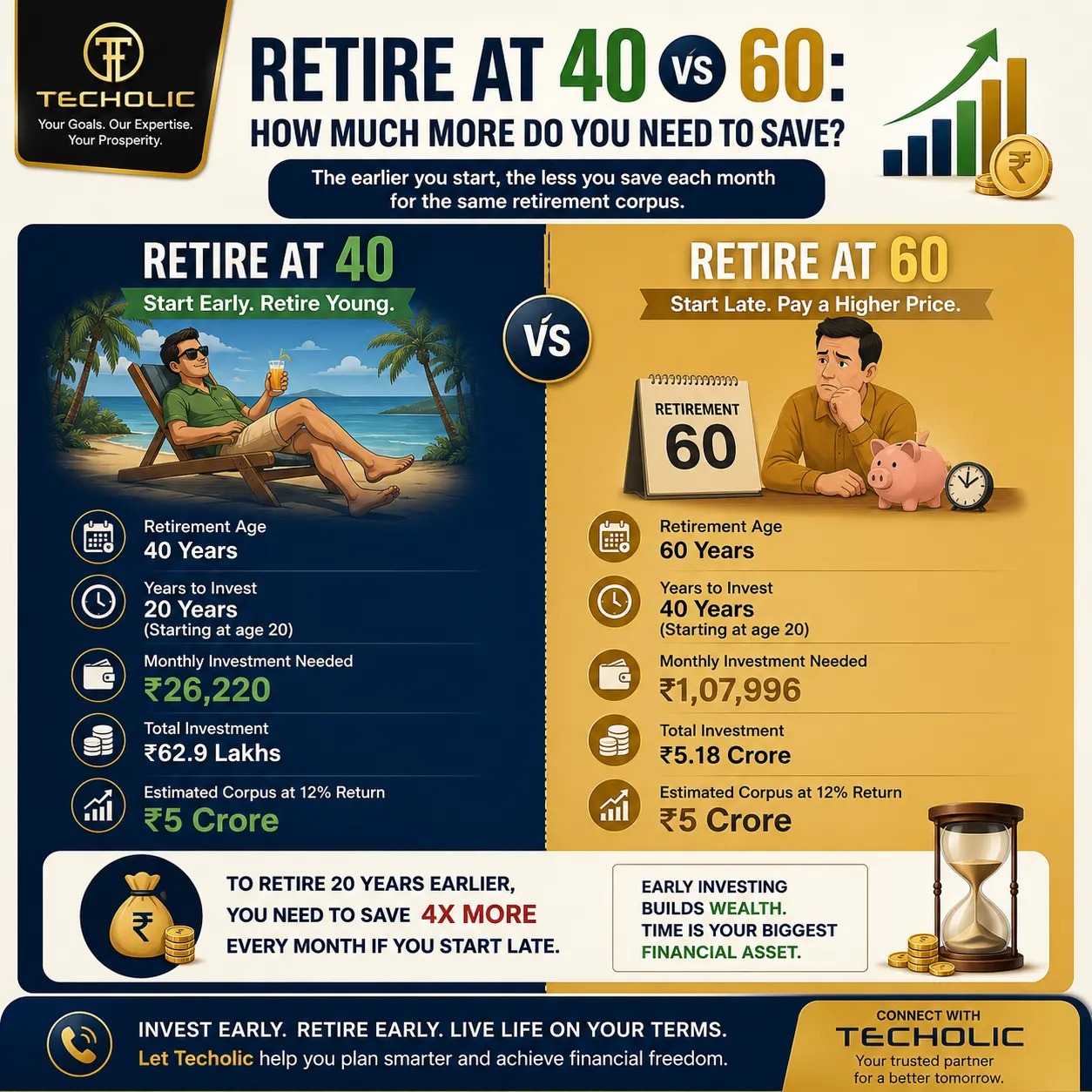

- Your accumulation period shrinks dramatically. If you start working at 23, you have only 17 years to build your corpus for a 40-year retirement, versus 37 years to build a corpus for a 60-year retirement.

-

- Your retirement duration nearly doubles. A 40-year-old retiree in India, with current life expectancy trends, needs to plan for 40-45 years of post-retirement life. A 60-year-old retiree typically plans for 20-25 years.

-

- You lose access to several retirement-specific benefits early. EPF withdrawal rules, pension payouts, and senior citizen tax benefits are all designed around the 58-60 age bracket. Retiring at 40 means self-funding everything without those structural supports for two more decades.

- Inflation has more time to work against you. A corpus that looks comfortable today gets quietly eroded over 40+ years if it’s not invested correctly.

-

This is why a sound investment strategy matters more for early retirement than almost any other financial goal. Get it wrong, and you either run out of money in your 60s, or you never actually pull the trigger on retiring early because the number always feels just out of reach.

How Much Corpus Do You Actually Need?

The starting point for any retirement plan — early or otherwise — is figuring out your annual expenses and working backward. The most commonly used method is the 25x rule (also called the 4% withdrawal rule), though for early retirement in India, we usually recommend adjusting it.

The 25x Rule, Explained Simply

If your annual expenses today are ₹6 lakh, the 25x rule says you need a corpus of ₹6 lakh × 25 = ₹1.5 crore to retire, assuming you withdraw 4% of your corpus annually and the rest stays invested and grows.

This rule works reasonably well for a 25-30 year retirement horizon. But if you’re retiring at 40, your money needs to last 40+ years, not 25. That changes things.

Why Early Retirees Need a Lower Withdrawal Rate

For a 40-year retirement horizon, most planners recommend a 3% to 3.5% withdrawal rate instead of 4%, simply because the money has to survive longer and absorb more market cycles, inflation shocks, and unexpected expenses (healthcare being the big one).

Using a 3.3% withdrawal rate, the math changes to roughly 30x your annual expenses instead of 25x.

Example:

-

-

- Annual expenses: ₹6 lakh

-

- Retire at 60 (25x rule): Corpus needed = ₹1.5 crore

- Retire at 40 (30x rule): Corpus needed = ₹1.8 crore

-

At first glance, that doesn’t look like a massive jump — just ₹30 lakh more. But this is where most people get the comparison wrong, because the bigger difference isn’t in the corpus size. It’s in the time you have to build it.

The Real Difference: Time, Not Just Money

This is the part that actually surprises people. Let’s compare two professionals, both currently 25 years old, both with the same ₹6 lakh annual expense lifestyle.

| Factor | Retire at 60 | Retire at 40 |

|---|---|---|

| Years to save | 35 years | 15 years |

| Corpus needed | ₹1.5 crore (25x) | ₹1.8 crore (30x) |

| Approx. monthly SIP needed (12% return assumption) | ₹6,000–7,000/month | ₹55,000–65,000/month |

| Retirement duration to plan for | 20–25 years | 40–45 years |

That SIP jump — from roughly ₹6,500 to over ₹60,000 per month — is the real story. You don’t need double the corpus. You need almost 10x the monthly investment discipline, because compounding simply hasn’t had enough time to do the heavy lifting.

This is exactly why a generic “save more” plan doesn’t work for early retirement. You need a structured investment strategy that front-loads aggressive equity exposure, automates consistency, and increases contributions as income grows.

What You Actually Have to Do to Retire at 40

If the goal is real, here’s what the plan typically looks like for someone serious about retiring 20 years earlier than the norm.

1. Calculate Your Real Number (Not a Round Figure)

Don’t just pick ₹2 crore or ₹5 crore because it sounds impressive. Work out:

-

-

- Your current annual expenses

-

- Expected lifestyle inflation (most people underestimate this)

-

- Healthcare costs as you age (a major blind spot — see below)

- Any one-time goals (child’s education, a second home, travel)

-

Add a buffer of at least 15-20% to your final number. Underestimating is the single most common — and costly — mistake in early retirement planning.

2. Maximize Equity Allocation Early

With only 15-20 years to build the corpus, you can’t afford to be conservative early on. A higher allocation to equity mutual funds — particularly diversified equity and index funds — gives compounding the room it needs to work. Debt instruments and fixed deposits, while safer, simply won’t generate the growth required in a compressed timeline.

A common allocation for someone targeting 40-year retirement in their late 20s:

-

-

- 70-80% equity (diversified large-cap, flexi-cap, and index funds)

-

- 15-20% debt (for stability and rebalancing opportunities)

- 5-10% alternative assets (gold, REITs, or international funds for diversification)

-

3. Increase SIPs Every Year, Not Just Start One

A flat SIP that never grows is one of the biggest reasons early retirement plans fail. As income rises, the SIP amount should rise with it — this is called a step-up SIP, and it’s arguably more important than the initial amount you start with.

Example: Starting a ₹20,000/month SIP and increasing it by 10% every year reaches a meaningfully larger corpus over 15 years than a flat ₹35,000/month SIP that never increases — while actually being easier on your monthly budget in the early years.

4. Don’t Ignore Tax-Efficient Structuring

Early retirees lose access to many of the tax benefits available to 60-year-old retirees (senior citizen FD rates, certain pension scheme benefits, etc.). This makes tax-efficient investing during the accumulation phase even more important — using equity mutual funds for long-term capital gains treatment, structuring withdrawals smartly, and timing redemptions to minimize tax drag.

5. Build a Healthcare Buffer Most People Forget

This is the single most underestimated cost in early retirement planning. At 60, you’re closer to senior citizen health schemes and shorter remaining life expectancy. At 40, you need health insurance and a dedicated medical buffer that has to last 40+ years, often without employer-provided coverage. A separate health corpus — not lumped into your general retirement number — is non-negotiable.

Retire at 40 vs 60 — Pros and Cons

Retiring at 40

Pros

-

-

- Decades of freedom to pursue passion projects, travel, or part-time work on your own terms

-

- More physical health and energy to actually enjoy retirement

- Forces disciplined investing habits early in life

-

Cons

-

-

- Requires an aggressive, near-flawless savings rate for 15-20 years

-

- Higher risk of corpus depletion if returns underperform expectations

-

- Loses access to employer benefits, group insurance, and certain government schemes early

- Less margin for error — a major financial setback in your 30s can derail the entire timeline

-

Retiring at 60

Pros

-

-

- Longer accumulation period means lower monthly investment burden

-

- Access to EPF, gratuity, pension benefits, and senior citizen tax slabs

- More time to recover from financial setbacks (job loss, market crashes, medical emergencies)

-

Cons

-

-

- Less healthy years left to enjoy retirement

-

- Inflation has more time to erode purchasing power if not planned correctly

- Risk of “one more year” syndrome — continuously delaying retirement past the original target

-

Common Mistakes People Make When Planning Early Retirement

-

-

- Using the same 25x rule for a 40-year retirement as they would for a 60-year one — this consistently underestimates the required corpus.

-

- Ignoring healthcare inflation, which historically runs higher than general inflation in India.

-

- Keeping the SIP amount flat instead of stepping it up with income growth.

-

- Being too conservative too early, parking money in FDs and debt funds when there are still 15+ years to ride out equity volatility.

-

- Not stress-testing the plan against a market downturn happening right after retirement — sequence-of-returns risk is real and can significantly impact early retirees.

- Forgetting children’s education and marriage costs while focusing solely on the retirement number.

-

How Techolic Helps You Plan This Out

At Techolic, we work with professionals across Chandigarh, Mohali, and Panchkula who are serious about early retirement — not as a vague dream, but as a calculated investment strategy with real numbers behind it. Every situation is different: your current expenses, risk appetite, dependents, and existing investments all change what your actual target should look like.

Rather than relying on generic online calculators that don’t account for India-specific factors like healthcare inflation, tax treatment, or regional cost-of-living differences, working with an investment advisor who understands your full financial picture helps you build a realistic, stress-tested plan — one that adjusts as your income, goals, and market conditions change over the years.

If you’re seriously considering retiring at 40 or 45 instead of 60, the earlier you build the right investment strategy, the more compounding works in your favor. Techolic can help you run the actual numbers based on your expenses, current savings, and risk profile, rather than ballpark figures from a generic article.

Frequently asked questions

Is it realistic for a middle-class Indian professional to retire at 40?

It’s realistic, but only with high savings discipline — typically saving 50-60% of income consistently for 15-20 years, combined with an aggressive equity-heavy investment strategy. It’s significantly harder for those who start saving seriously only in their early 30s.

How much monthly SIP do I need to retire at 40 with a ₹5 lakh/month expense lifestyle?

For a high-expense lifestyle like this, the corpus required (using the 30x rule) would be roughly ₹18 crore. Starting at age 25 with a 15-year timeline and assuming 12% annual returns, this would require a SIP in the range of ₹4-5 lakh per month, or a smaller starting SIP with aggressive annual step-ups and rising income.

Should I use the 4% withdrawal rule or 3% for early retirement?

What’s the biggest risk in retiring at 40 instead of 60?

Sequence-of-returns risk — a market downturn in the first few years after retirement can significantly damage a corpus that still has 40+ years left to last. This is why asset allocation and withdrawal strategy matter as much as the corpus size itself.

Can I retire at 40 with just mutual funds, or do I need other investments too?

Mutual funds, particularly equity-oriented ones, typically form the core of an early retirement investment strategy due to their growth potential and liquidity. However, a well-rounded plan usually also includes health insurance, an emergency fund, some debt allocation for stability, and possibly real estate or other assets depending on individual goals.

Does retiring early mean I stop earning completely?

Not necessarily. Many people who retire early choose semi-retirement — consulting, part-time work, or passion projects that generate some income. This reduces the pressure on the corpus and is often a more realistic middle ground than a complete stop to all income.