Choosing the right health insurance plan is one of the most important financial decisions for Indian families today. With rising medical inflation, unpredictable health emergencies, and increasing lifestyle-related illnesses, having adequate health cover is no longer optional—it’s essential.

One of the most common questions people face while buying health insurance is:

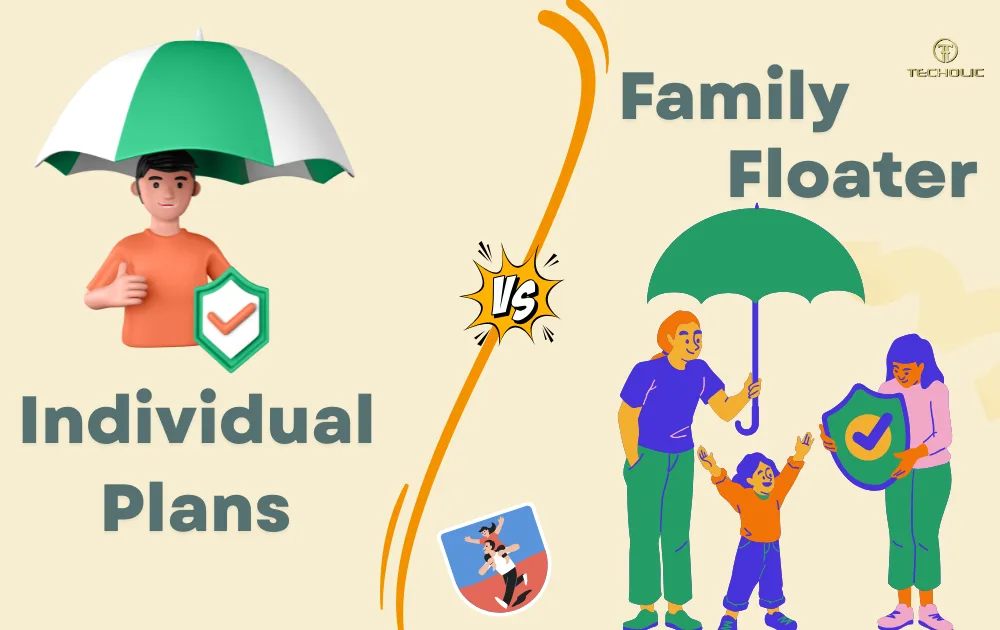

Should I choose a Family Floater Policy or Individual Health Insurance Plans?

Both options serve the same purpose—covering medical expenses—but they work very differently. This guide will help you understand each plan clearly, compare costs and benefits, and choose the option that best suits your family’s needs.

Understanding the Basics of Health Insurance Plans

Before comparing the two, let’s first understand how each plan works.

What Is a Family Floater Health Insurance Policy?

A family floater policy covers multiple family members under one single sum insured. This sum insured can be used by any insured member, either fully or partially, during the policy year.

Example:

If you buy a family floater plan with a ₹10 lakh cover for yourself, your spouse, and your child, the entire ₹10 lakh is shared among all three members. If one member uses ₹4 lakh, the remaining ₹6 lakh is still available for others.

Who is usually covered:

- Self

- Spouse

- Dependent children

- In some plans, dependent parents (recommended separately)

What Is an Individual Health Insurance Plan?

An individual health insurance plan provides separate coverage for one person. Each insured member has their own sum insured, independent of others.

Example:

If you, your spouse, and your child each have individual plans of ₹5 lakh, every member has their own dedicated ₹5 lakh coverage, regardless of others’ claims.

Key Differences Between Family Floater and Individual Plans

1. Coverage Structure

- Family Floater: One shared sum insured for all members

- Individual Plan: Separate sum insured for each member

This difference plays a major role during multiple hospitalizations in the same year.

2. Premium Cost Comparison

Family Floater Premiums

- Generally lower and more cost-effective for young families

- Premium is mainly calculated based on the eldest member’s age

Individual Plan Premiums

- Higher overall cost if buying multiple policies

- Premium depends on each person’s age, health condition, and coverage amount

Cost Insight:

For young couples with children, a family floater is usually more economical. However, as age or medical risk increases, individual plans may offer better value.

3. Suitability Based on Family Type

Family Floater Is Ideal If:

- You have a young nuclear family

- All members are below 45–50 years

- No major pre-existing medical conditions

- Hospitalizations are expected to be infrequent

Individual Plans Are Better If:

- Family members have different age groups

- Parents or senior citizens are involved

- Someone has pre-existing health conditions

- You want guaranteed coverage for each person

Most financial advisors in India recommend separate individual plans for parents, even if you choose a floater for self, spouse, and children.

Risks and Limitations to Consider

Risks in a Family Floater Plan

- One large claim can exhaust the entire sum insured

- Other family members may remain uncovered until renewal

- Premium increases significantly as the eldest member ages

Risks in Individual Plans

- Higher total premium for multiple members

- Managing multiple policies can be slightly more complex

Tax Benefits Under Indian Income Tax Laws

Both family floater and individual health insurance plans qualify for tax deductions under Section 80D of the Income Tax Act.

- Up to ₹25,000 for premiums paid for self, spouse, and children

- Additional ₹25,000 for parents (₹50,000 if parents are senior citizens)

- Maximum deduction can go up to ₹1,00,000

Tax benefits remain the same regardless of which plan type you choose.

Flexibility and Long-Term Value

Adding Family Members

- Family Floater: Easier mid-term addition of spouse or newborn child

- Individual Plan: New member usually requires a separate policy

Customisation Through Riders

Both plans allow add-ons such as:

- Critical illness cover

- Hospital cash benefit

- Waiting period reduction

- Restore or recharge benefit

Portability

As per IRDAI guidelines, you can port both family floater and individual plans to another insurer while retaining waiting period benefits.

Practical Examples to Help You Decide

Scenario 1: Young Couple with a Child

A family floater plan of ₹10–15 lakh offers better value and flexibility at a lower premium.

Scenario 2: Family with Senior Citizen Parents

Individual plans for parents + family floater for self, spouse, and children is the safest approach.

Scenario 3: Member with Pre-existing Condition

An individual plan ensures that one person’s health condition doesn’t affect coverage for others.

Key Takeaways: Which One Should You Choose?

There is no one-size-fits-all answer. The right choice depends on:

- Age of family members

- Health conditions

- Budget

- Long-term medical needs

Quick Rule of Thumb:

- Go for a family floater for young, healthy families

- Choose individual plans for senior citizens or high-risk members

- A combination of both often works best in Indian households

Conclusion: Make a Choice Based on Protection, Not Just Price

Health insurance is not just about saving money—it’s about ensuring uninterrupted access to quality healthcare without financial stress. While family floater plans offer cost efficiency, individual plans provide certainty and dedicated protection.

Evaluate your family’s health profile today, not just current expenses. The right decision now can save you from major financial strain in the future.

Before buying, assess your family structure, compare benefits carefully, and choose a plan that offers long-term security, not just short-term savings. If needed, consult a trusted insurance advisor to tailor coverage to your family’s real needs.