If you’ve ever opened a mutual fund app and seen four options sitting next to each other — Direct Growth, Direct IDCW, Regular Growth, Regular IDCW — and felt a jolt of confusion, you’re not alone. We get this question almost every week from clients who assumed “growth” and “direct” were the same thing, only to realize they answer two completely different questions.

This mix-up isn’t a minor detail. Picking the wrong combination can quietly cost you lakhs over a 15-20 year horizon. So let’s clear this up properly.

Direct vs Regular and Growth vs IDCW Are Two Separate Decisions

Here’s the part most articles skip, and it’s exactly why this confuses people: a direct growth mutual fund isn’t one category. It’s the answer to two independent questions stacked together.

Question 1: Who are you buying the fund from?

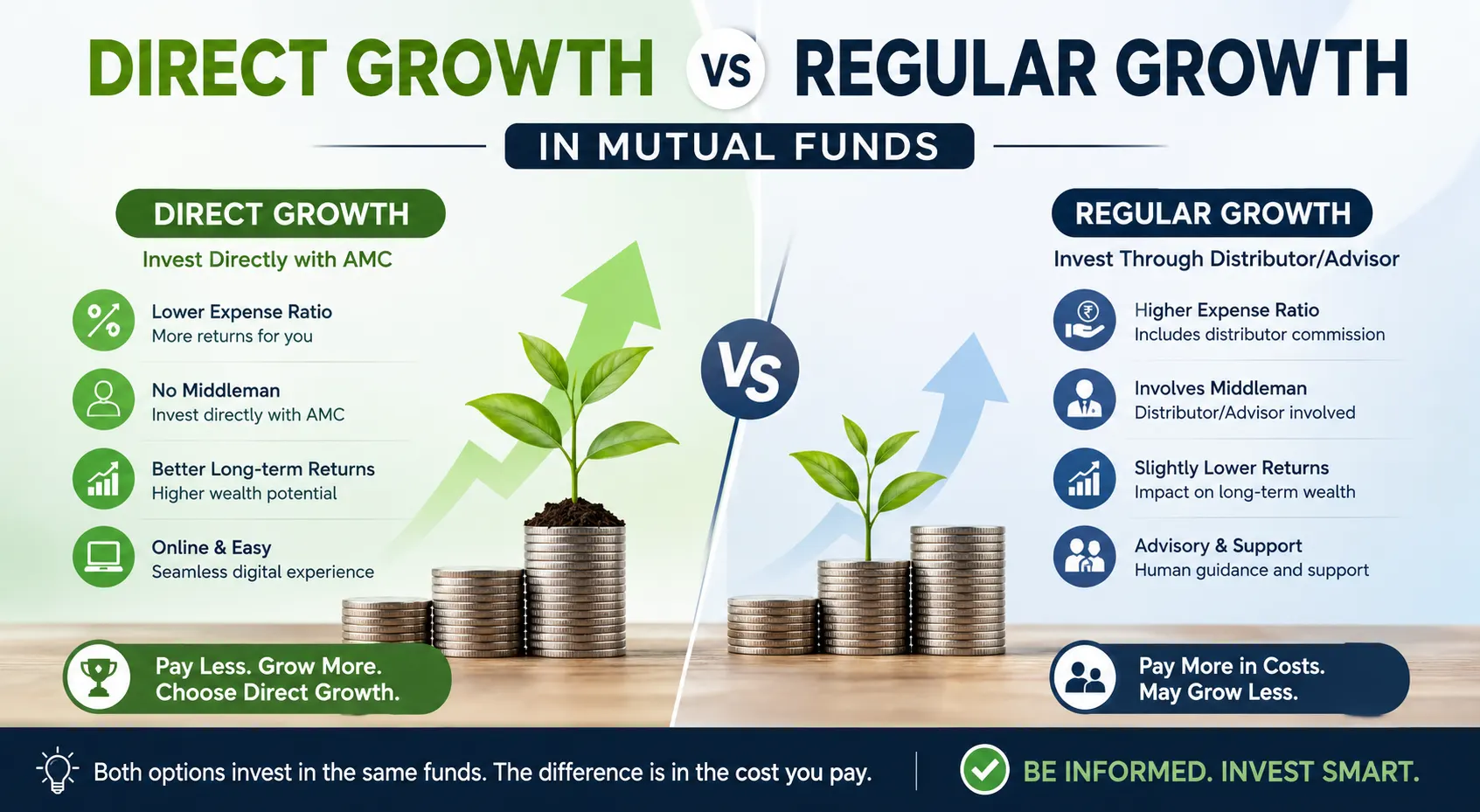

- Direct Plan — you invest straight through the AMC’s website, an RTA like CAMS, or a platform like Coin/Kite, with no distributor in between

- Regular Plan — you invest through a distributor, broker, or advisor who earns a trail commission from the AMC for bringing you in

Question 2: What happens to the profit the fund generates?

- Growth Option — profits stay invested and compound inside the fund; your unit price (NAV) rises over time, and you only realise the gain when you redeem

- IDCW Option (Income Distribution cum Capital Withdrawal, earlier called “Dividend”) — the fund periodically pays out a portion of profits to you in cash, and your NAV drops by that same amount after each payout

So when someone searches for a direct growth mutual fund, they’re really asking about a combination: no distributor commission (Direct) + profits reinvested rather than paid out (Growth). You could just as easily have a Regular Growth fund, a Direct IDCW fund, or a Regular IDCW fund — all four combinations exist for almost every scheme.

Why Does This Matter for Your Actual Returns?

Each choice affects your money differently, and conflating them is where most confusion — and cost — comes from.

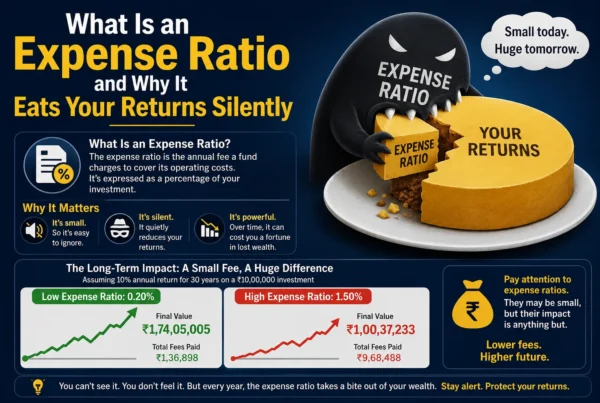

Direct vs Regular affects your expense ratio. Under the SEBI (Mutual Funds) Regulations, 2026, effective from April 1, 2026, AMCs now disclose the Base Expense Ratio separately from statutory levies like GST and STT, making this cost gap even easier to see. A regular plan’s expense ratio includes the distributor’s trail commission — typically 0.5% to 1% higher than the equivalent direct plan. On a large-cap equity fund, that often means paying around 1.0% (direct) versus 1.7-1.8% (regular) every year, regardless of performance.

Growth vs IDCW affects your taxation and cash flow. Every IDCW payout is added to your taxable income that financial year. A Growth option defers any tax event until you redeem your units, so your money compounds tax-free in the interim and you control when you trigger a tax liability.

Together, this is why a direct growth mutual fund is the default recommendation for most long-term, wealth-building investors in India: it minimises the annual fee drag and defers taxation until you choose to exit.

A Real Numbers Example: ₹15,000 SIP for 20 Years

Let’s say you start a ₹15,000 monthly SIP at age 30, expecting a 12% annual return before costs, and run it for 20 years.

- Regular Growth fund (expense ratio ~1.7%): effective return drops to roughly 10.3% after costs, taking your corpus to approximately ₹1.32 crore.

- Direct Growth fund (expense ratio ~0.9%): effective return comes to roughly 11.1% after costs, taking your corpus to approximately ₹1.51 crore.

That’s a gap of nearly ₹19 lakh — purely from the expense ratio difference, with the Growth option held constant on both sides. Choose IDCW instead, and you’d also be paying tax on every payout along the way, widening this gap further.

What Were the Doubts Investors Usually Have Here?

Is direct growth mutual fund always the cheaper option?

Yes, between Direct and Regular for the same scheme, Direct always carries a lower expense ratio, since it has no distributor commission built in. This holds true across every AMC and fund category.

If direct is cheaper, why does regular growth still exist?

Regular plans bundle in the distributor’s advisory service — fund selection, rebalancing reminders, paperwork support. For someone who wants that hand-holding and is willing to pay the trail commission for it, regular plans aren’t a mistake; they’re a trade-off.

What does “direct growth” mean exactly, when I see it on an app?

It means two filters have both been applied: plan type is “Direct” (no distributor) and option type is “Growth” (profits reinvested, no payouts). You’ll see it written as “Scheme Name – Direct Plan – Growth Option” in the factsheet.

Can I switch from regular growth to direct growth later?

Yes, but it’s treated as a redemption and fresh purchase, which can trigger capital gains tax if your units have appreciated. Weigh the tax cost of switching against the long-term savings, ideally with proper guidance.

Does direct growth mean higher returns than regular growth from the same fund?

The underlying portfolio and fund manager are identical in both plans. The only difference is the expense ratio deducted before computing NAV, so a direct growth mutual fund shows a marginally higher NAV over time — purely due to lower cost, not better fund management.

Common Mistakes Investors Make With This Choice

- Assuming “growth” means high-risk and “direct” means risky DIY investing — neither is true; growth just means reinvested profits, and direct just means no distributor commission. Risk depends on the underlying asset class, not the plan or option type.

- Choosing IDCW for “regular income” without checking the tax impact — many retirees pick IDCW assuming it behaves like fixed deposit interest, without realising it’s taxed and the payout isn’t guaranteed.

- Switching to direct growth without checking exit load and capital gains — saving 0.7% annually is great, but not if a hasty switch triggers a tax bill bigger than several years of savings.

- Going direct with no plan for review or rebalancing — the savings only pay off if you stay invested through volatility with a clear strategy.

Direct Growth vs Regular Growth: A Quick Side-by-Side

Who buys it: Direct Growth is bought straight from the AMC or RTA platform; Regular Growth is bought through a distributor or advisor.

Expense ratio: Direct Growth runs lower, typically by 0.5% to 1% depending on the fund category; Regular Growth carries the added distributor commission.

Profit treatment: Both Direct Growth and Regular Growth reinvest profits into the NAV — this part is identical, since “Growth” is the option, not the plan type.

Tax timing: Both defer tax until redemption, since neither pays out IDCW along the way.

Best suited for: Direct Growth suits investors who do their own research or work with a fee-based advisor; Regular Growth suits investors who want ongoing distributor support bundled into the cost.

Making the Right Call for Your Portfolio

The direct growth mutual fund route makes mathematical sense for almost every long-term investor — the cost savings compound exactly like your returns do. But “cheaper” doesn’t automatically mean “right for you” if you have no system for reviewing your portfolio or deciding when to switch funds.

This is exactly where we come in. At Techolic, we help clients access direct plans while still getting the portfolio reviews and goal-tracking that regular plans are usually bought for — so you’re not choosing between cost and guidance, you’re getting both.

Compare your direct vs regular mutual fund holdings with our advisory team and find out exactly how much you could be saving — without giving up the guidance you need.

Frequently Asked Questions

1. What is the main difference between direct growth and regular growth mutual funds? Direct growth funds are bought without a distributor and carry a lower expense ratio; regular growth funds are bought through a distributor who earns a trail commission, resulting in a higher expense ratio. Both reinvest profits the same way.

2. Which gives better returns, direct growth or regular growth? Direct growth typically delivers slightly better returns over the long term, purely because of the lower expense ratio. The fund manager and portfolio are identical in both cases.

3. Is it safe to invest directly without a distributor? Yes, direct plans are equally SEBI-regulated and safe. The “risk” some investors associate with going direct is really about lacking guidance for fund selection, not the safety of the investment itself.

4. How do I check if my mutual fund is direct or regular? Your Consolidated Account Statement (CAS) from CAMS or KFintech clearly lists the plan type — “Direct” or “Regular” — alongside “Growth” or “IDCW” for each holding.

5. Should beginners choose direct growth mutual fund options? Beginners can choose direct growth if they’re comfortable researching funds themselves or working with a fee-only advisor. If you’d prefer built-in support without paying separately for advice, a regular plan with a trusted advisor is a reasonable starting point.